Roughly 1 in 4 Canadians cannot cover an unexpected $500 expense, and 85% now say living paycheque to paycheque feels like the new normal. The gap between what Canadians have saved and what a real emergency costs has rarely been wider.

This is the most current snapshot of Canadian emergency-fund data for 2026. We pulled every figure that matters from Statistics Canada, the Financial Consumer Agency of Canada, Angus Reid, H&R Block, and other primary sources, with United States numbers at the end for comparison. Canadian data comes first, and every stat links to its original source.

Key Takeaways

- 26% of Canadians cannot cover an unexpected $500 expense, according to Statistics Canada.

- Only 55% of Canadians had an emergency fund covering three months of expenses in 2024, down from 64% in 2019.

- 85% of Canadians say living paycheque to paycheque is the new norm, up from 60% a year earlier.

- A majority of Canadians under 55 could not handle a sudden $1,000 expense without borrowing.

- 48% of Canadians lean on credit cards instead of savings, while payday lenders charge 365% to 391% APR.

- Advisors recommend three to six months of expenses, but most experts say to start with a $500 to $1,000 starter fund first.

Emergency Fund Statistics, Trends & Data in Canada

Canadians are more exposed to a financial shock than the headline economy suggests. Here is what the data says about who can cover an emergency, who has a fund, and how that breaks down by age, region, and gender.

How Many Canadians Can Cover an Emergency Expense?

Statistics Canada data shows 26% of Canadians cannot cover an unexpected $500 expense, more than 1 in 4 households. The share rises sharply for younger and lower-income Canadians, leaving most with little room for a surprise bill.

- 26% of Canadians could not cover an unexpected expense of $500. This is the most recent official figure, from the Statistics Canada Canadian Social Survey, with fall 2022 data. Roughly 1 in 4 households has no easy way to handle a small emergency. (Statistics Canada)

- 35% of Canadians reported difficulty meeting their household financial needs in the prior year. The same survey found more than a third struggled to cover transportation, housing, food, and other essentials. (Statistics Canada)

- A majority of Canadians under 55 could not handle a sudden $1,000 expense. Polling from the Angus Reid Institute found financial resilience for younger and middle-aged Canadians slipped back toward pre-pandemic lows. (Angus Reid Institute)

- 45% of renters say a $250 unexpected expense would strain their finances, compared with 29% of mortgage holders. Renters carry far less of a cushion than owners. (Angus Reid Institute)

- 53% of Canadians could cover a $1,000 emergency without borrowing. Among the rest, 15% would reach for a credit card, 10% would borrow from family or friends, and 8% would use a line of credit. (Finder)

- 28% of Canadians would dip into an emergency fund to handle a $1,000 expense. Fewer than 3 in 10 have savings set aside specifically for that purpose. (Finder)

How Many Canadians Have an Emergency Fund?

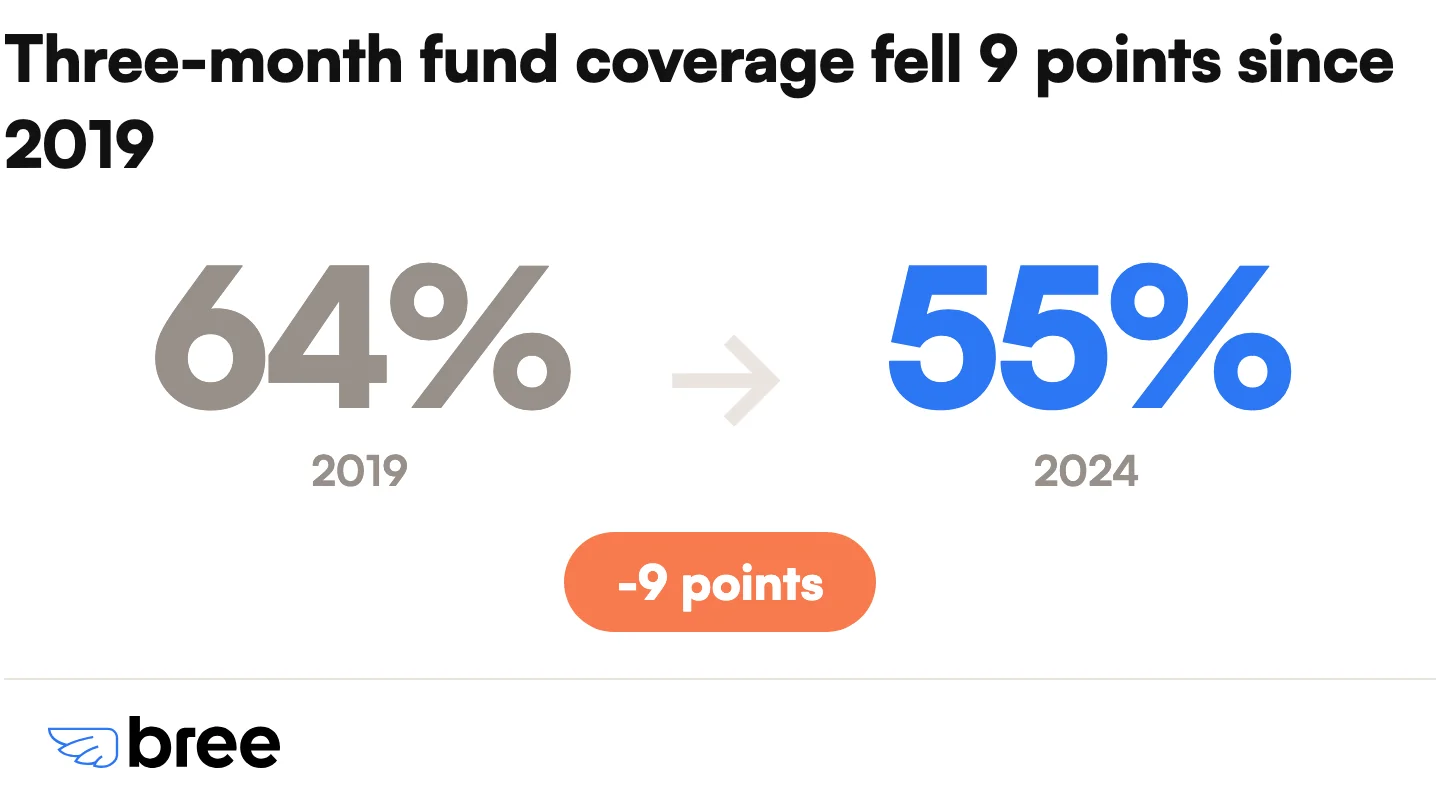

Only 55% of Canadians had an emergency fund covering three months of expenses in 2024, down from 64% in 2019, according to Financial Consumer Agency of Canada data reported by Scotiabank. The share of Canadians with a real cushion has been falling for years.

- 55% of Canadians had an emergency fund covering three months of expenses in 2024, down from 64% in 2019. The Financial Consumer Agency of Canada data, reported by Scotiabank, shows preparedness dropped nine points in five years. (Scotiabank)

- 49% of Canadians had no savings set aside for an emergency in a 2019 survey. This older Refresh Financial and Leger poll found nearly half the country with no buffer, and 35% who said they would turn to a loan or credit card. Treat it as a historical marker, not a current reading. (Advisor.ca)

- 45% of Canadians lacked an emergency fund in an earlier CIBC poll from 2012. The figure is more than a decade old, but it shows the gap is not new. By age, 60% of those 45 to 64 had a fund versus 51% of those 18 to 44. (Advisor.ca)

Emergency Savings by Age and Generation

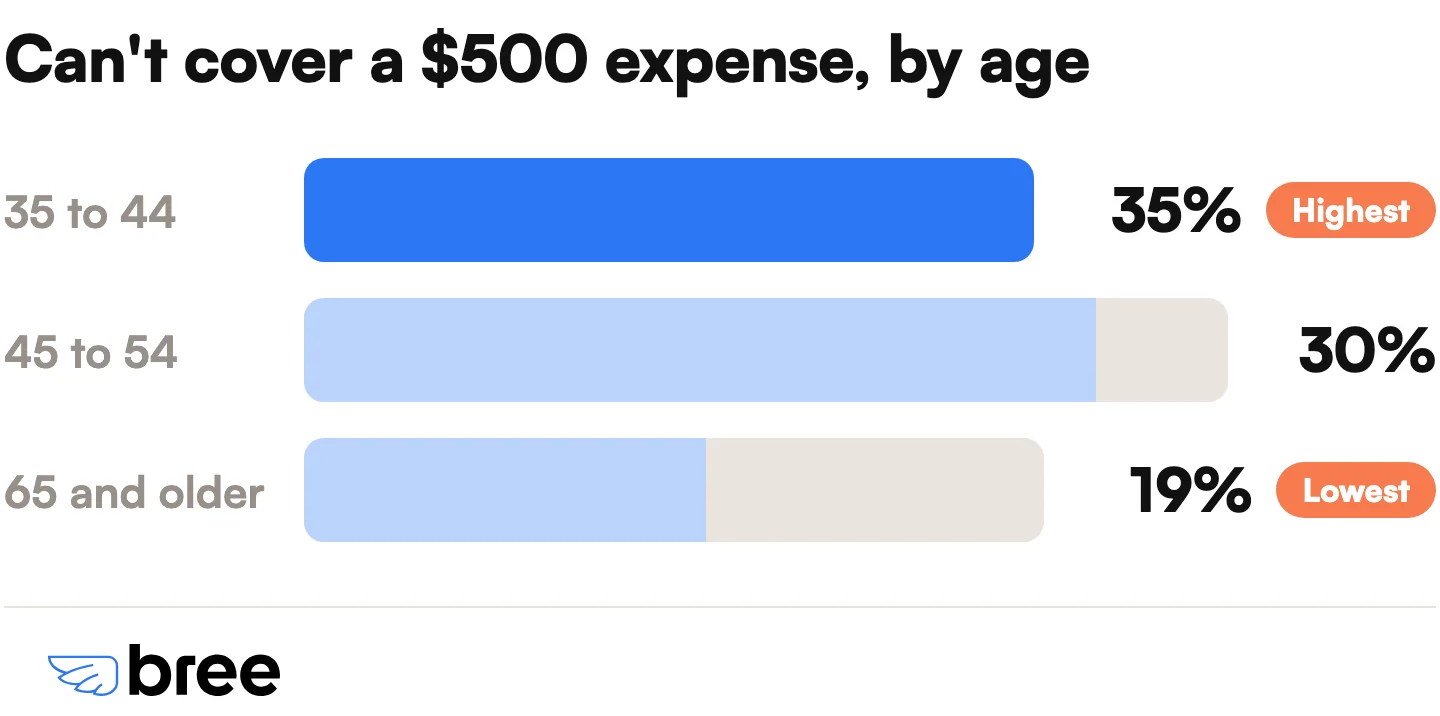

Younger Canadians are the most exposed. The share that cannot cover a $500 expense peaks in the prime working years, when childcare, rent, and debt payments hit hardest.

- 35% of Canadians aged 35 to 44 cannot cover a $500 expense, the highest of any age group. (Statistics Canada)

- 30% of Canadians aged 45 to 54 cannot cover a $500 expense. The pressure stays high through middle age before easing in retirement. (Statistics Canada)

- 19% of Canadians aged 65 and older cannot cover a $500 expense, the lowest of any group. Fixed retirement income and lower housing costs leave seniors more stable than younger workers. (Statistics Canada)

- Median financial assets for Canadians under 35 sit near $7,600, versus about $30,000 for those 65 and older. These are general savings, not strictly emergency funds, but they show how little younger households have on hand. (MoneySense)

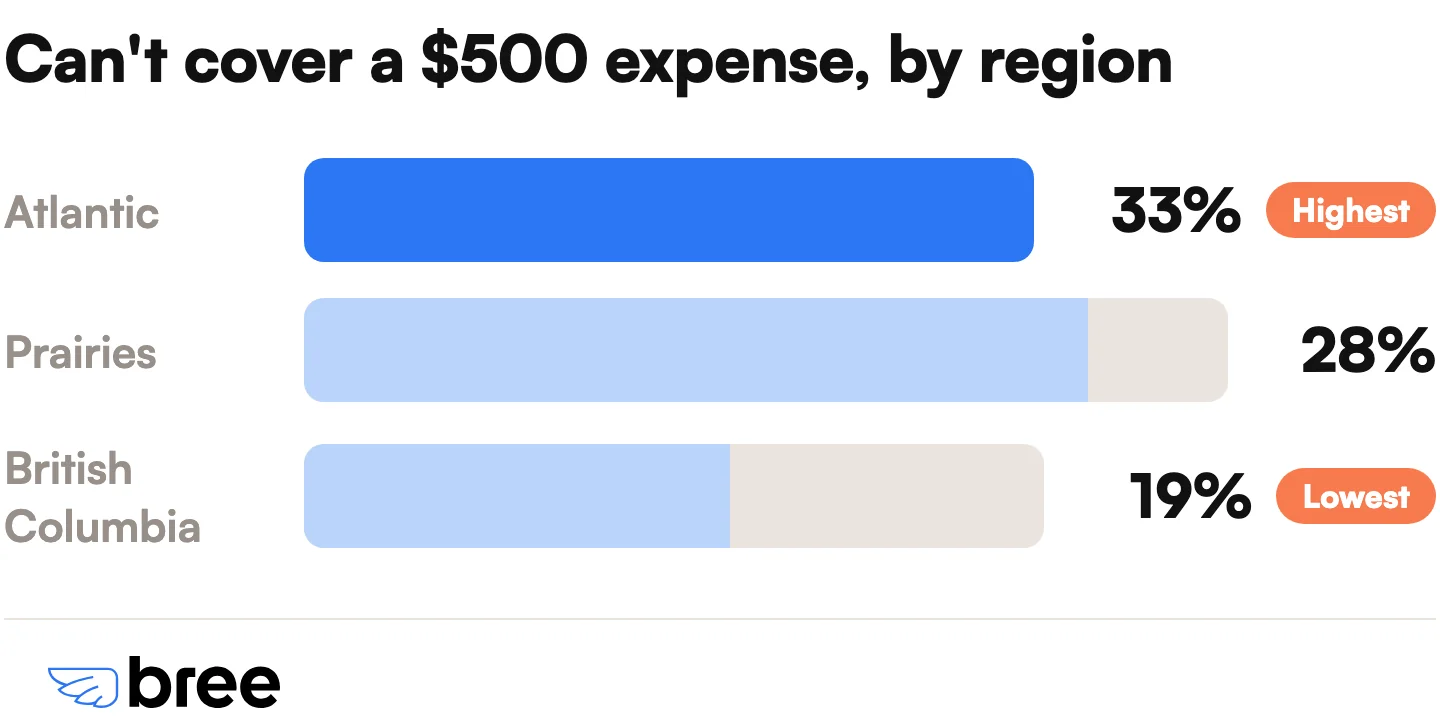

Emergency Preparedness by Region and Population Group

Where Canadians live shapes how prepared they are. Atlantic Canada is the most stretched, British Columbia the least.

- 33% of Atlantic Canadians cannot cover a $500 expense, the highest regional figure. The Prairies follow at 28%, and British Columbia is lowest at 19%. (Statistics Canada)

- 51% of Black Canadians could not cover a $500 expense, compared with 14% of non-racialized, non-Indigenous Canadians. Filipino Canadians were at 38% and Chinese Canadians at 14%, showing wide gaps by population group. (Statistics Canada)

Emergency Savings by Gender

Women carry slightly less of a financial cushion than men, a pattern that holds in both Canadian and US data.

- 29% of Canadian women cannot cover a $500 expense, compared with 24% of men. The five-point gap reflects wider differences in income and caregiving costs. (Statistics Canada)

How Long It Takes Canadians to Build a Fund

Building an emergency fund takes most Canadian renters years, not months. Research found 71% of renters in Canadian cities would need up to 24 months to save one, as high housing costs swallow the money that would otherwise go to savings.

- 71% of renters in Canadian cities would need up to 24 months to save a full emergency fund. Rent leaves little room to set money aside in most major markets.

- Vancouver renters spend about 43% of after-tax income on rent. With average rent near $2,534 against after-tax income of $5,883, saving an emergency fund there is especially hard.

Why So Many Canadians Can't Save

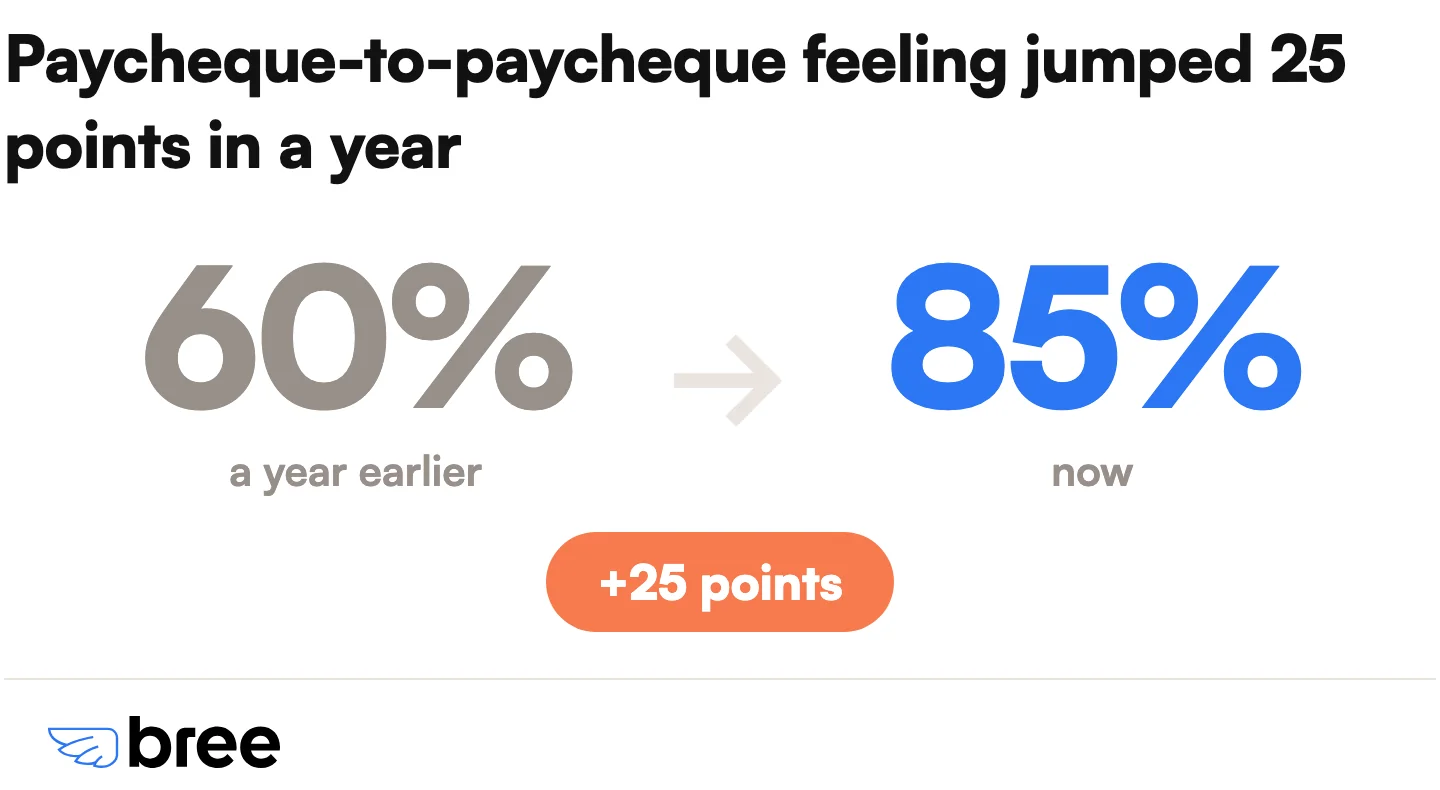

85% of Canadians say living paycheque to paycheque now feels like the norm, up from 60% a year earlier, according to H&R Block Canada. The savings gap tracks the rising cost of living and shrinking room in household budgets, not a lack of discipline.

- 85% of Canadians say living paycheque to paycheque is the new norm, up from 60% a year earlier. This H&R Block Canada survey is the headline number on financial fragility in the country right now. (H&R Block Canada)

- 56% of Canadians worry they would have to go into debt for an unexpected expense rather than use savings. More than half expect to borrow, not draw down a fund, when a surprise bill lands. (H&R Block Canada)

- 74% of Canadians worry they aren't putting enough into savings, and 78% expect to have less to save this year. The anxiety is widespread and getting worse, not better. (H&R Block Canada)

- 42% of Canadians cite money as their top source of stress. Financial worry outranks work, health, and relationships in the FP Canada Financial Stress Index. (FP Canada)

- 68% of Canadians name the high cost of living as the top barrier to financial progress. Grocery prices and inflation lead the list of external pressures squeezing budgets. (FP Canada)

- The Canadian household saving rate fell to 4.4% in late 2025, down from 5.2% the prior quarter. Households are setting aside a smaller slice of income than a year ago. (Statistics Canada via Trading Economics)

- 44% of Canadians are very concerned about affording their housing or rent. Shelter cost is the single biggest drain on the budget that would otherwise build a fund. (Statistics Canada)

What Canadians Do When They Don't Have an Emergency Fund

Without a cushion, a surprise bill turns into debt. The data shows most Canadians fall back on credit cards, and the most exposed fall back on far costlier options.

- 48% of Canadians lean on credit cards for larger purchases instead of tapping savings, and 17% use buy-now-pay-later plans. Borrowing has quietly replaced saving as the default emergency plan. (H&R Block Canada)

- 35% of Canadians without a fund said they would use a loan or credit card to cover an emergency. That 2019 survey figure has only grown more relevant as savings rates fall. (Advisor.ca)

- Payday lenders in Canada charge the equivalent of 365% to 391% APR. For someone with no fund, a short-term payday advance is one of the most expensive ways to cover a $500 gap. (Financial Consumer Agency of Canada)

- Overdraft and non-sufficient-funds (NSF) fees long ran $45 to $48 per incident in Canada. A federal cap lowered NSF fees to $10 as of March 2026, but repeat charges still stack up when an account runs dry before payday. (Financial Consumer Agency of Canada)

This is the gap a cash advance is built to close. Bree is an instant cash advance app in Canada that offers interest-free advances of up to $750 with no credit check and no late fees, and it accepts government benefits like ODSP, OW, CPP, CCB, and EI as income. For a Canadian facing a $500 surprise before payday, that is a 0% APR alternative to payday loans and a higher limit than apps that cap advances at $250. More than 600,000 Canadians have used it to bridge the gap while they rebuild savings. A cash advance is not a long-term fix, but it keeps a one-time emergency from turning into high-interest debt.

How Much Should You Have in an Emergency Fund?

Financial advisors recommend keeping three to six months of essential expenses in a liquid, easy-to-access account. Most experts tell Canadians to start smaller and build up.

- Advisors generally recommend three to six months of essential expenses in an emergency fund. The money should sit in a liquid account such as a high-interest savings account or a Tax-Free Savings Account (TFSA), not locked in investments. (Federal Reserve Bank of St. Louis)

- Most financial guidance suggests starting with a smaller $500 to $1,000 starter fund before targeting the full three to six months. A reachable first goal is what gets most people started, then they build from there (Federal Reserve Bank of St. Louis). The free FCAC Financial Goal Calculator can map a savings timeline.

For a step-by-step plan on where to keep the money and how to automate it, see our guide on why you should have an emergency fund.

Frequently Asked Questions

What percentage of people have an emergency fund?

In Canada, 55% of people had an emergency fund covering three months of expenses in 2024, down from 64% in 2019 (Scotiabank). In the United States, about 46% of adults have at least three months of expenses saved, while 24% have no emergency savings at all (Bankrate).

How many Canadians have $10,000 or more in savings?

Hard data on this exact threshold is limited. The median Canadian under 35 holds about $7,600 in financial assets, rising to roughly $30,000 for those 65 and older, so most younger households sit well below $10,000 in accessible savings (MoneySense). Total balances vary widely by age and income.

Is $20,000 too much for an emergency fund?

It depends on your monthly expenses. The standard target is three to six months of essential costs. For a household spending about $3,300 a month, $20,000 covers roughly six months, which sits at the high end of the recommended range. For lower expenses, $20,000 may be more than you need, and the extra could work harder in a TFSA or paying down high-interest debt.

What is the 3-6-9 rule for an emergency fund?

The 3-6-9 rule is a tiered savings goal. Three months of expenses is the minimum cushion, six months is comfortable for most households, and nine months suits people with variable or self-employed income who face less predictable cash flow.

The Bottom Line

The data points one direction: most Canadians are underprepared for a financial shock, and the cushion is shrinking. A quarter of the country cannot cover a $500 expense, only 55% have three months of savings, and 85% feel they live paycheque to paycheque. The gap between what households have saved and what an emergency costs is widening, not closing.

Building a fund takes time, and most Canadians do not have it set aside today. Bree gives Canadians an interest-free cash advance of up to $750 to cover an unexpected bill, so a $500 surprise does not turn into 391% payday-loan debt while you rebuild your savings. It is a cash advance, not a loan, with no credit check and no late fees.

If a bill lands before payday, you can get up to $750 to cover the gap and pay it back on your next deposit, then keep building toward a real cushion.

Sources

- Statistics Canada: Canadian Social Survey, financial impacts

- Angus Reid Institute: savings and financial resilience

- Finder: Canadian personal finance statistics

- Scotiabank: emergency fund advice and FCAC data

- Advisor.ca: Canadians and financial plans for emergencies

- Advisor.ca: half of Canadians don't have emergency savings

- MoneySense: how much the average Canadian has in savings

- H&R Block Canada: paycheque-to-paycheque survey

- FP Canada: Financial Stress Index

- Statistics Canada via Trading Economics: household saving rate

- Zoocasa: renters and emergency funds

- Financial Consumer Agency of Canada: payday loans

- Financial Consumer Agency of Canada: NSF fee regulations

- Federal Reserve Bank of St. Louis: emergency fund guidance

- Bankrate: Emergency Savings Report

- Empower: emergency savings research

- Federal Reserve: economic well-being of US households

- Yahoo Finance: Americans and emergency savings gaps

Join our newsletter to get the latest updates

.png)

.png)