Most Canadians say they were never taught how to handle money. Nearly two-thirds finished school without a single personal finance lesson, and it shows in the numbers: confidence runs high, but real knowledge lags behind. Canada ranks near the top of the world on paper, yet the gaps fall hardest on women, young people, newcomers, and households with the least room to absorb a mistake. Below are some of the most current financial literacy statistics in Canada, grouped by theme and sourced to the original research.

Key Takeaways

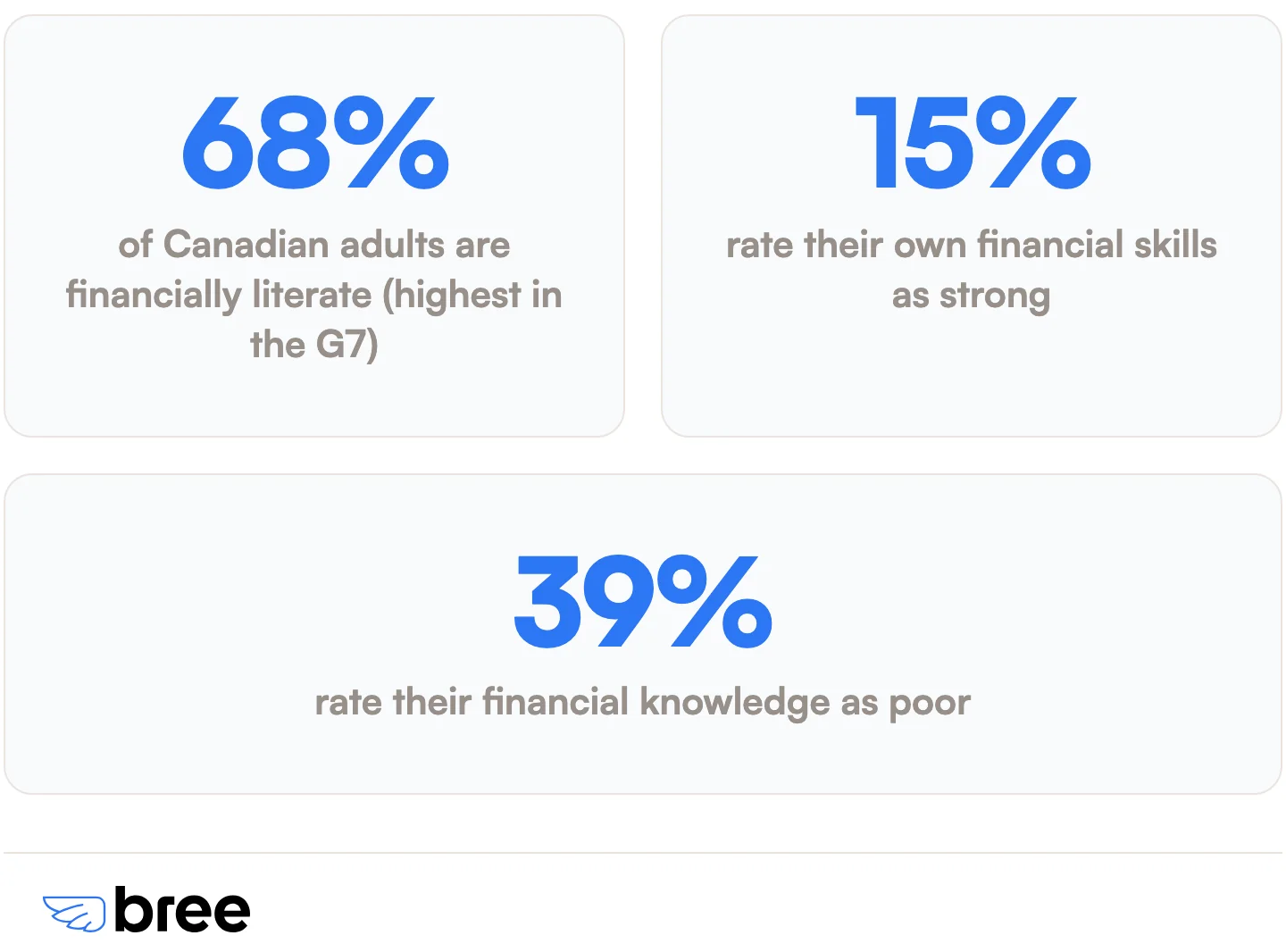

- 68% of Canadian adults are financially literate, the highest rate in the G7 (S&P Global FinLit Survey).

- Only 15% of Canadians rate their financial skills as strong, while 39% call them poor (MNP Consumer Debt Index).

- 64% of Canadians never learned money management in school (Edward Jones survey via Investment Executive).

- 49% of Canadians keep a budget, up from 46% a decade earlier (FCAC Canadian Financial Capability Survey).

- 40% of credit-seeking Canadians did not know a payday loan is the most expensive way to borrow (Loans Canada).

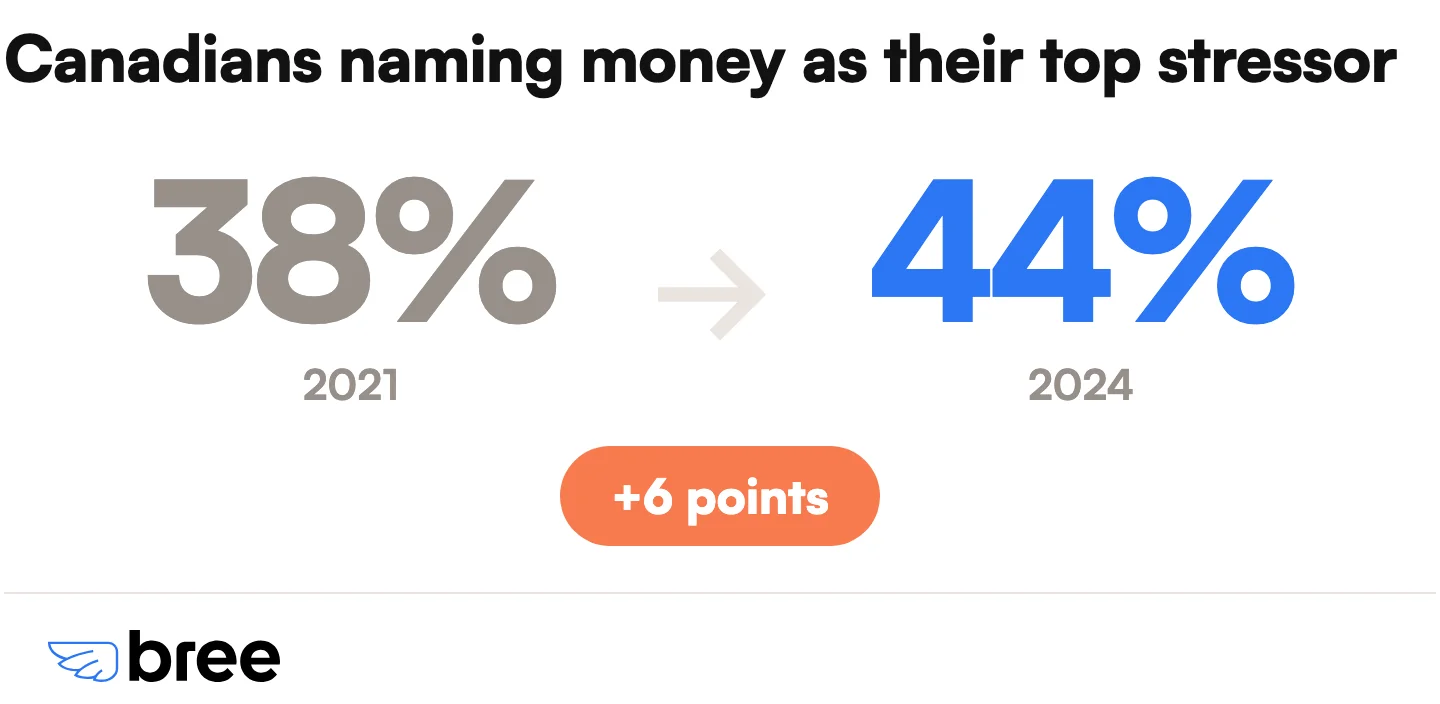

- 44% of Canadians say money is their leading source of stress (FP Canada Financial Stress Index).

- Canadian 15-year-olds scored 519 in financial literacy, 21 points above the OECD average (OECD PISA via CMEC).

How Financially Literate Are Canadians?

Canada has one of the highest financial literacy rates in the world, but most Canadians still rate their own knowledge as weak. The headline figures look strong, while the self-reported numbers tell a more honest story.

1. 68% of Canadian adults are financially literate, the highest rate in the G7. This put Canada ahead of every other G7 country in the largest global study of its kind, which surveyed more than 150,000 adults across 140-plus economies (S&P Global FinLit Survey).

2. Only about 33% of adults worldwide are financially literate. Two-thirds of adults globally cannot answer basic questions about interest, inflation, and risk, which makes Canada's rate look strong by comparison (S&P Global FinLit Survey).

3. Just 15% of Canadians believe they have strong financial literacy skills. Another 39% rate their financial knowledge as poor, a self-assessment gap that sits well below the country's global ranking (MNP Consumer Debt Index).

4. Only 49% of Canadians keep a household budget, up from 46% a decade earlier. Barely half of households track their spending, one of the most basic money-management habits (FCAC Canadian Financial Capability Survey).

Financial Literacy by Age and Generation

Younger Canadians score lower on financial knowledge but are more likely to admit they need help. The generational gap shows up in test scores, debt stress, and the willingness to ask for support.

5. Younger Canadians consistently score lower on financial literacy than older generations. Gen Z and younger millennials post the weakest results on national knowledge measures, while older adults tend to score highest, a pattern federal researchers link to less hands-on experience with major financial decisions (Government of Canada financial literacy research).

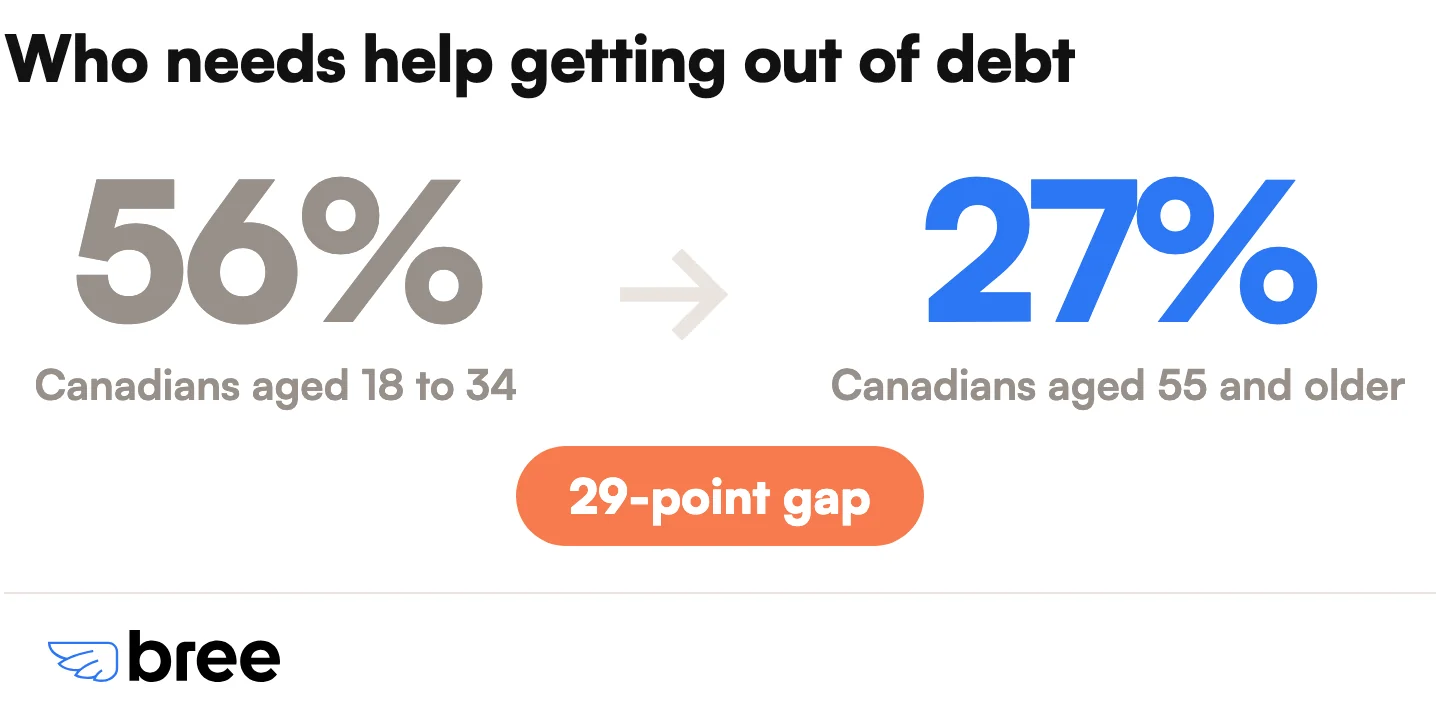

6. 56% of Canadians aged 18 to 34 say they need help getting out of debt, versus 27% of those 55 and older. Younger adults are roughly twice as likely to feel stuck with debt (Ipsos for MNP).

7. 61% of Canadians aged 18 to 34 feel embarrassed about the idea of bankruptcy, compared with 34% of those 55 and older. The shame around money problems is far heavier for younger Canadians (Ipsos for MNP).

8. 55% of Canadians aged 25 to 44 say rising prices greatly affect their daily expenses, versus 28% of seniors. Cost-of-living pressure lands hardest on younger working-age adults (Statistics Canada).

Youth and Student Financial Literacy

Canadian teenagers rank among the strongest in the world on financial literacy tests, and the gender gap that appears in adults has not yet formed. The school-age numbers are some of the most encouraging in the country.

9. Canadian 15-year-olds scored 519 on the OECD financial literacy assessment, 21 points above the OECD average. That placed Canadian students near the top of participating countries, alongside Denmark and the Netherlands (OECD PISA via CMEC).

10. Only 13% of Canadian students fell below the baseline level of financial literacy, compared with 18% across the OECD. Fewer Canadian teens struggle with the basics than the international average (OECD PISA via CMEC).

11. There was no average gender gap in youth financial literacy in Canada. Boys and girls scored about the same, unlike the gap that appears in adult surveys (OECD PISA via CMEC).

12. Eight Canadian provinces took part in the OECD youth financial literacy assessment. Alberta, British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, and Prince Edward Island all participated (OECD PISA via CMEC). For ways to build on those early skills, see our guide to financial education resources in Canada.

The Gender Gap in Financial Literacy

Canadian men score higher than women on financial knowledge tests, but a large part of the gap comes from women being more likely to answer "don't know." The split shows up across every core topic.

13. Canadian men scored 62.2% on a financial knowledge quiz, versus 58.6% for women. The 3.6-point gap held across a national survey of financial capability (Statistics Canada).

14. 21.5% of men answered all five key financial knowledge questions correctly, compared with 14.7% of women. Fewer than one in six women got a perfect score on questions covering interest, inflation, and risk (Statistics Canada).

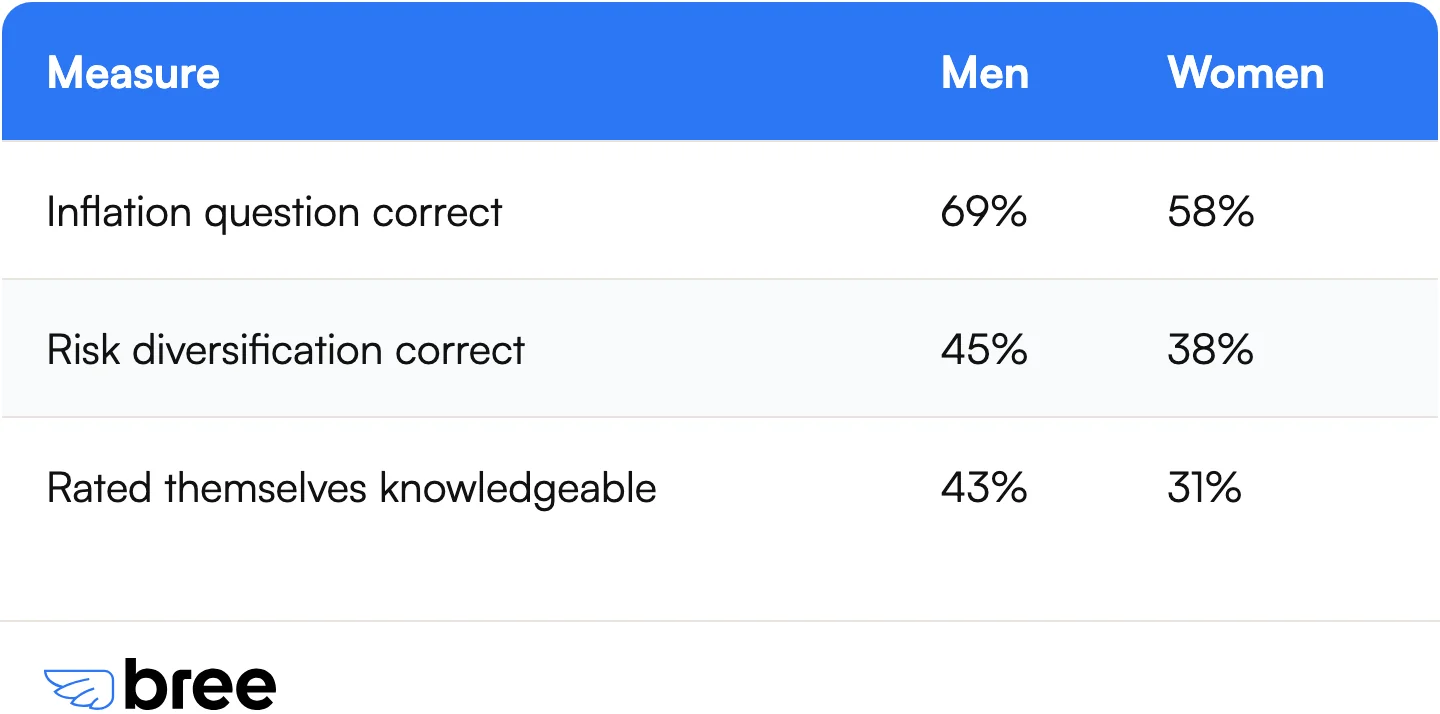

15. On the inflation question, 69% of men answered correctly versus 58% of women. Understanding how rising prices erode purchasing power showed one of the wider gaps (Statistics Canada).

16. On risk diversification, 45% of men answered correctly versus 38% of women. The idea that spreading money across investments lowers risk tripped up most respondents of either gender (Statistics Canada).

17. 43% of men rated themselves financially knowledgeable, versus 31% of women. The confidence gap was wider than the actual knowledge gap (Statistics Canada).

18. Women were more likely to answer "don't know" to a knowledge question, at 45% versus 32% for men. Part of the measured gap reflects how each group responds when unsure, not only what they know (Statistics Canada).

The "Big Three" Questions Most People Get Wrong

Financial literacy researchers measure knowledge using three core questions, often called the "Big Three," covering interest, inflation, and risk diversification. Most adults worldwide cannot answer all three.

19. The "Big Three" questions test compound interest, inflation, and risk diversification. Economists Annamaria Lusardi and Olivia Mitchell developed them as a quick measure of whether someone understands the basics of money (Global Financial Literacy Excellence Center).

20. Only about 30% of adults globally answer all three "Big Three" questions correctly. Roughly one-third of older adults understand interest, inflation, and risk diversification together, even in wealthy countries (Global Financial Literacy Excellence Center).

Financial Education in Canadian Schools

Most Canadians went through school without any money lessons, and the majority wish they had. Several provinces are now making personal finance a required part of the curriculum.

21. 64% of Canadians did not learn about money management in school. Nearly two-thirds entered adulthood without formal personal finance education (Edward Jones via Investment Executive).

22. 84% of Canadians believe learning about money in school would have helped them manage their finances with less stress. The appetite for earlier financial education is nearly universal (Edward Jones via Investment Executive).

23. Ontario will require students to pass a Grade 10 financial literacy test to graduate, starting in 2026. Students must score at least 70% on the assessment, making Ontario one of the first provinces to tie graduation to money knowledge (Government of Ontario).

24. Only three provinces, Quebec, Ontario, and Saskatchewan, have mandatory personal finance components in their curriculum. The rest fold money topics into broader subjects without a dedicated requirement (Government of Ontario).

25. Every province and territory except New Brunswick and the Northwest Territories includes or plans to include financial literacy in school curricula. Coverage is widening, though the depth still varies widely by region (Government of Ontario).

Confidence vs. Competence: The Real Literacy Gap

Canadians who got even a little money education in school feel far more capable than those who did not. The data shows confidence is closely tied to early exposure, not just raw knowledge.

26. 78% of Canadians who learned at least a bit about money in school rate their skills as good, versus 59% of those who did not. Early exposure to personal finance has a lasting effect on how capable people feel (Edward Jones via Investment Executive).

27. 41% of Canadians with no school financial education rate their money skills as "okay at most," versus 22% of those who had some. People who missed out on money lessons are nearly twice as likely to feel shaky about their abilities (Money.ca).

28. 67% of credit-seeking Canadians claimed high confidence in their financial decisions, despite large gaps in their actual knowledge. Confidence often outran competence in a study of Canadians applying for credit (Loans Canada).

Financial Literacy, Debt, and High-Cost Borrowing

Lower financial literacy lines up closely with expensive borrowing and debt stress. The Canadians who know the least about money are the most likely to pay the most for it.

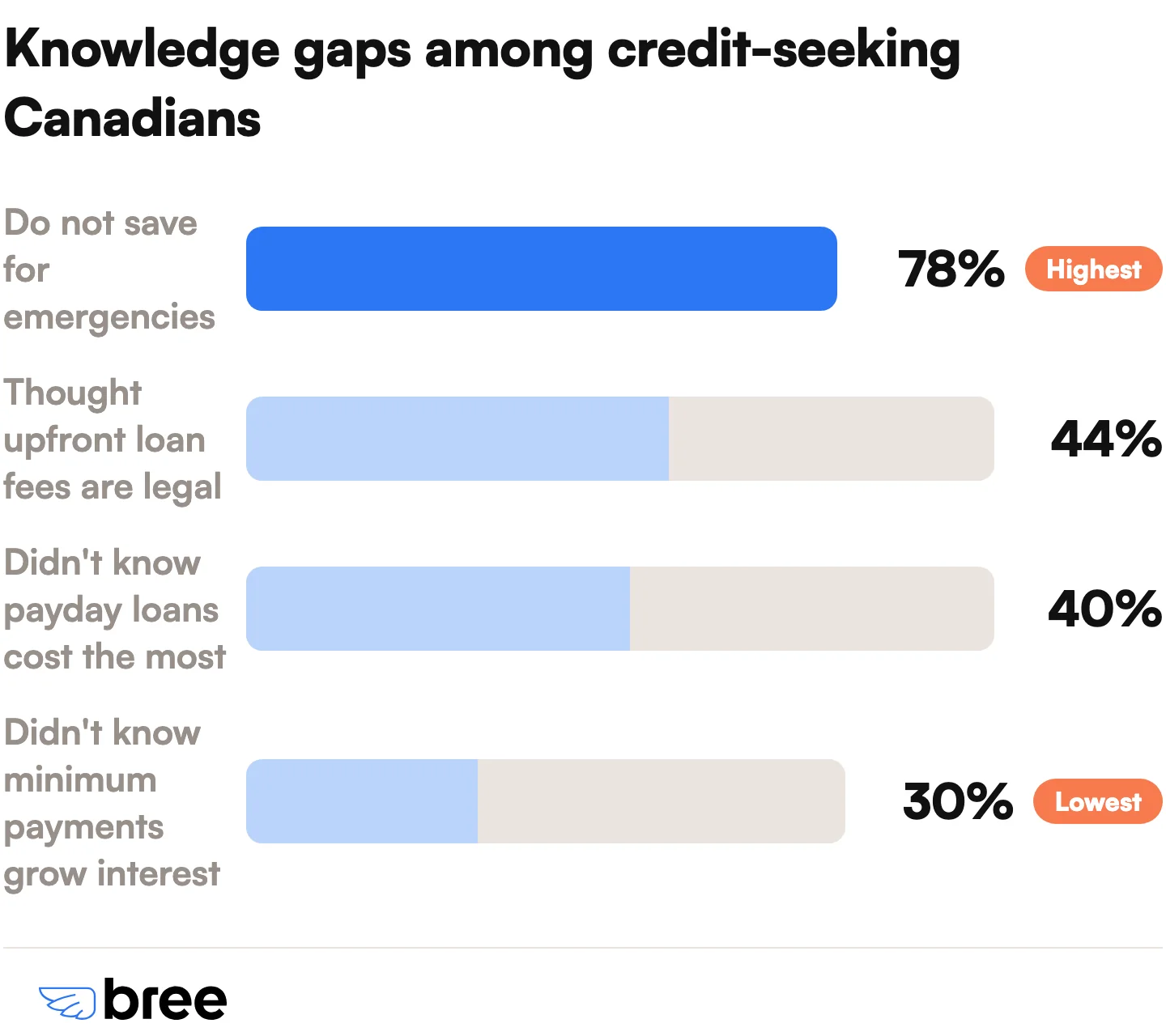

29. 40% of credit-seeking Canadians did not know a payday loan is the most expensive way to borrow. Many people turn to high-cost credit without realizing cheaper options exist (Loans Canada).

30. 30% of credit-seeking Canadians did not know that paying only the credit card minimum still leaves interest to pile up. A basic misunderstanding of credit card interest keeps balances growing (Loans Canada).

31. 44% of credit-seeking Canadians wrongly believed it is legal for a lender to charge upfront fees before issuing a loan. This misconception leaves people open to advance-fee scams (Loans Canada).

32. 78% of credit-seeking Canadians do not save for emergencies. The lack of a cushion pushes more people toward borrowing when an unexpected cost hits (Loans Canada). For why that cushion matters, see our guide on why you should have an emergency fund.

33. The higher Canadians rate their financial literacy, the fewer payday loans they take out. Financial regulators found this pattern held across every area of financial knowledge they measured (FCAC payday loan research).

34. 43% of Canadians say they need help getting out of debt. The share rose as debt stress climbed alongside higher living costs (Ipsos for MNP).

35. 36% of Canadians do not know how to get out of debt or where to turn for help. That figure climbed six points since the previous survey, a sign the knowledge gap is widening (Ipsos for MNP).

This is where low literacy gets expensive. A payday loan in Canada can carry an effective annual rate of 365% to 391%, and many people reach for one simply because they do not know the alternatives. Bree closes part of that gap with a different model: its advances charge 0% interest, run no credit check, and treat government benefits such as CPP, EI, and ODSP as qualifying income, up to a limit of $750. If you are trying to break the cycle, start with our guide to escaping the payday loan debt cycle or see how an interest-free cash advance works.

Financial Stress and Well-Being in Canada

Money is the single biggest source of stress for Canadians, and that stress spills into sleep, work, and life satisfaction. Financial worry has climbed steadily over the past several years.

36. 44% of Canadians say money is their top source of stress, up from 38% in 2021. Finances rank ahead of work, health, and relationships as the leading stressor (FP Canada Financial Stress Index).

37. 49% of Canadians lose sleep over financial worries. Nearly half report that money stress disrupts their rest (FP Canada Financial Stress Index).

38. Only 17% of highly financially stressed Canadians report high life satisfaction, versus 70% of those with no money stress. The link between financial strain and overall well-being is stark (Statistics Canada).

39. Canadians who work with a financial professional are more hopeful about their future, at 60% versus 48% who do not. Guidance, not just income, shapes how people feel about money (FP Canada Financial Stress Index Report).

Retirement is a particular blind spot: nearly 69% of Canadian adults do not know how much they need to save for it (debt.ca). These pressures land on already-stretched budgets, with roughly four in five Canadians (85%) saying they live paycheque to paycheque, per an H&R Block Canada survey. When budgets are that tight, small knowledge gaps turn into expensive mistakes.

Financial Literacy Among Newcomers and Indigenous Canadians

Financial literacy gaps fall hardest on groups that already face barriers in the financial system. Newcomers and Indigenous Canadians both report lower knowledge and less access than the general population.

40. Newcomers report lower financial knowledge and higher financial anxiety than Canadian-born adults. Federal research indicates that language barriers and unfamiliar financial systems leave many recent immigrants less confident navigating credit, banking, and government benefits (Government of Canada financial literacy research).

41. An estimated 15% of people in First Nations communities are unbanked, roughly double the rate for non-Indigenous Canadians. Limited access to mainstream banking pushes more reliance on costly alternatives like payday lenders (Prosper Canada). Federal research names low-income earners, youth, women, newcomers, and Indigenous Peoples as the groups most in need of tailored financial education (Government of Canada).

Financial Literacy by Province

Debt stress and the need for help vary by province, with the Prairies and Ontario reporting some of the highest demand for support. Regional differences show financial literacy is not a single national story.

In Alberta, 51% of residents say they need help getting out of debt, and 58% distrust professional debt-help companies (Ipsos for MNP). In Ontario, 49% say they need debt help. Provincial differences also showed up in youth results, where the eight participating provinces posted a range of scores on the OECD financial literacy assessment. For region-specific guidance, see our guide on improving your financial health in Alberta.

How Canada Compares to the Rest of the World

Canada ranks among the most financially literate countries, but "best in a struggling field" is the honest framing. Most adults worldwide cannot pass a basic financial knowledge test.

Within the G7, financial literacy ranges from 37% in Italy to 68% in Canada, the highest in the group (S&P Global FinLit Survey). Globally, two-thirds of adults are not financially literate, and a significant gender gap exists in nearly every economy studied. On the youth side, the OECD average financial literacy score sits near 498, while Canada's 519 places it near the top alongside Denmark and the Netherlands (OECD PISA via CMEC).

Frequently Asked Questions

What percentage of Canadians are financially literate?

About 68% of Canadian adults meet a basic financial literacy standard, the highest rate in the G7, according to the S&P Global FinLit Survey. Self-assessment is lower, though: only 15% of Canadians rate their own skills as strong.

Is Canada financially literate compared to other countries?

Yes, relative to the rest of the world. Canada has the highest financial literacy rate in the G7 at 68%, according to the S&P Global FinLit Survey. Canadian teenagers also scored 21 points above the OECD average on the youth financial literacy assessment.

What is the 50/30/20 rule in financial literacy?

The 50/30/20 rule splits your after-tax income into three buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It is one of the simplest budgeting frameworks for beginners. Our full guide explains how to budget with the 50/30/20 rule.

What are the 5 C's of financial literacy?

The 5 C's are a lending framework used to judge creditworthiness: character, capacity, capital, collateral, and conditions. Lenders weigh these five factors when deciding whether to extend credit and on what terms.

Why is financial literacy a problem in Canada?

The main issue is that most Canadians were never taught money management in school, with 64% reporting no formal financial education. That leaves a gap between how confident people feel and how much they actually know, which leads to costly mistakes with debt and high-interest borrowing.

The Bottom Line

Canada looks strong on the global scoreboard, but the everyday numbers tell a harder story. Most Canadians were never taught money in school, confidence outruns real knowledge, and the widest gaps fall on the people with the smallest financial cushion. Financial literacy is not just a school subject. It decides who pays 391% to borrow and who does not.

Closing that gap takes both better education and fairer tools for the moments when cash runs short. That second part is where Bree fits, giving Canadians between paycheques an instant cash advance at 0% APR instead of a triple-digit payday loan, with no credit check and government benefits counted as income. If a tight week has you weighing your options, you can see how a cash advance of up to $750 compares to high-cost borrowing.

Sources

- S&P Global FinLit Survey

- MNP Consumer Debt Index

- Edward Jones survey via Investment Executive

- Financial Consumer Agency of Canada: Review of Financial Literacy Research

- Ipsos for MNP: Canadians Need Debt Help

- Statistics Canada: Let's Talk About Money

- OECD PISA Financial Literacy via CMEC

- Statistics Canada: Financial Literacy and Retirement Planning

- Global Financial Literacy Excellence Center

- Government of Ontario: Financial Literacy Education in Schools

- Money.ca: Canadians Lack Financial Education

- Loans Canada: Financial Literacy vs Financial Well-Being

- FCAC: Understanding Payday Loan Use

- FCAC Canadian Financial Capability Survey

- FP Canada Financial Stress Index

- FP Canada Financial Stress Index Report

- Prosper Canada: Indigenous Financial Wellness

- H&R Block Canada

- Debt.ca: Canada's Financial Literacy Month

Join our newsletter to get the latest updates

.png)