People look for apps like NotchUp because they like the idea of fast cash between paycheques without a credit check, but they want a lower cost, wider availability, or a more proven track record. NotchUp advances a larger amount, but it charges a flat fee on every advance and is licensed in only one province.

This guide ranks six alternatives, shows what each one really costs, and explains who each app fits. Bree is a cash advance, not a loan, so there is no interest and no debt cycle by design.

Key Takeaways

- Bree leads on cost. Free standard delivery, 0% interest, and no late fees mean a $0 mandatory cost. You can borrow up to $750, and government benefits count as income.

- NotchUp's edge is the amount. It advances up to $1,500 and accepts gig and freelance income, but it charges a flat $5 per advance and its licence is centred in British Columbia.

- Most alternatives cap at $250. Nyble and KOHO Cover top out at $250. Bree's $750 limit is the tier that actually covers a real emergency.

- None of these apps run a credit check. Approval is based on your bank transaction history, not your credit score.

- Watch the real cost. Per-advance fees and monthly subscriptions add up, even in months you borrow nothing.

What Is NotchUp, and Why Look for Alternatives?

NotchUp is a Canadian earned wage access app that advances up to 50% of your next paycheque, capped at $1,500, for a flat $5 fee, with no credit check and no SIN required. Funds arrive by Interac e-Transfer in about 15 minutes, 24/7. According to Finder's NotchUp review, the app accepts a wide range of income types, including employment, freelance work, EI, CPP, ODSP, and CCB.

NotchUp has real strengths. The $1,500 ceiling is higher than most cash advance apps, the income flexibility is broad, and the e-Transfer is fast.

The reasons people search for alternatives are just as real. The flat $5 charge applies to every advance, so frequent use adds up. NotchUp holds a payday lender licence (number 86443) in British Columbia, yet advertises acceptance of incomes tied to other provinces, an inconsistency Finder flags directly. The app also has a thin and mixed review history, with recurring complaints about funding delays and weak customer support.

About 1 in 4 Canadians could not cover an unexpected $500 expense, according to Statistics Canada. When money is that tight, cost and reliability matter more than a higher ceiling you may never reach. If a clean record with no credit check is your priority, see our guide to cash advances without a credit check in Canada.

Quick Comparison: NotchUp vs the Best Alternatives

Amounts and terms are accurate as of June 2026 and can change. Always confirm current terms on each provider's site before you apply.

Top 6 Apps Like NotchUp in Canada

1. Bree: Best for Interest-Free Cash Advances

Bree is a Canadian cash advance app that offers up to $750 with 0% interest, no credit check, and no late fees. Standard delivery is free and arrives in 1 to 3 business days. Express delivery reaches your connected debit card in under 5 minutes for a small fee. There is no mandatory subscription, and the optional membership ($2.99/month, first month free) can be bypassed by sharing bank statements.

Bree accepts government benefits as qualified income, including ODSP, OW, CPP, CCB, and EI. This matters because some competitors and roundups wrongly claim Bree only accepts employment income. That is not correct. If your income comes from disability support, a pension, or child benefits, you can still qualify.

Trust is where Bree pulls ahead. The app holds a 4.8 out of 5 Trustpilot rating across 8,007+ reviews and has served 600,000+ Canadians. That is a far deeper track record than the newer apps on this list.

Pros:

- 0% interest, no late fees, free standard delivery

- Up to $750, higher than most app-based options

- Accepts government benefits as income

- No credit check

- 600,000+ users, 4.8 out of 5 Trustpilot

Cons:

- Max advance is $750, below NotchUp's $1,500

- Needs consistent deposits of at least $1,200 per month

Who it's for: Canadians who want a no-cost advance, accept that $750 covers most short gaps, and value a proven app. It is also the clear pick for anyone on government benefits.

Bree works well alongside benefit schedules. If your payment date and your bills do not line up, Bree can bridge the gap. See our guide to e-Transfer advances for ODSP recipients. You can get up to $750 interest-free and sign up in minutes.

2. Nyble: Best for Building Credit While You Borrow

Nyble offers advances up to $250 and doubles as a credit-builder that reports your payments to Equifax. There is no credit check to start. Standard delivery is free, while instant delivery runs through a paid monthly membership. The value here is not the amount, which is small, but the credit reporting.

The credit-builder angle is what sets Nyble apart. Each on-time repayment is reported to Equifax, so steady use can slowly lift a thin or damaged credit file over time. That is a different goal from covering an emergency. If your main aim is rebuilding credit, Nyble's Equifax reporting does more than a bigger advance would. If you need cash to cover a real shortfall, $250 may fall short, and an app like Bree that advances up to $750 fits better.

Pros:

- Reports payments to Equifax to help build credit

- No credit check to qualify

- Free standard delivery option

Cons:

- $250 cap is low for a true emergency

- Credit reporting matters only if that is your goal

Who it's for: Canadians focused on credit building who also want occasional small advances. For more options in this space, see our roundup of Nyble app alternatives in Canada.

3. KOHO Cover: Best for Existing KOHO Cardholders

.jpg)

KOHO Cover provides an overdraft-style advance of $20 to $250 with 0% interest on the advance itself. It requires both a KOHO account and a paid Cover subscription, so the 0% headline comes with a monthly cost attached. It only makes sense if you already use KOHO for everyday spending.

The advance is instant to your KOHO balance, which is convenient for existing users. For everyone else, opening a new account and paying a recurring subscription to reach $250 is a lot of setup for a small amount. Run the math on the monthly fee first. A subscription you pay every month can cost more over a year than a single flat advance fee elsewhere.

Pros:

- 0% interest on the advance

- Instant access for current KOHO users

Cons:

- Requires a KOHO account plus the Cover subscription

- $250 cap, same low ceiling as Nyble

Who it's for: People who already bank with KOHO and want a small cushion. If you are weighing KOHO against other apps, see our KOHO review and top alternatives.

4. Wagepay: Best for Larger Repeat Advances on Employment Income

.jpg)

Wagepay advances up to $1,500 for repeat users, matching NotchUp's ceiling. Unlike a true cash advance app, Wagepay charges a flat fee plus annual interest, which is a different cost model from a free or flat-fee advance. It is available mainly in British Columbia and Ontario and accepts employment income only.

The higher limit is the draw. The trade-off is cost. Charging both a fee and interest puts Wagepay closer to a short-term loan than a no-cost advance, so it pays to compare the total cost against a 0% option before you borrow.

Pros:

- Up to $1,500 for repeat users

- Same-day funding

Cons:

- Charges a fee plus interest

- Employment income only, limited provinces

Who it's for: Employed Canadians in BC or Ontario who need a larger amount and accept paying interest for it. For a closer look at this option, see our guide to apps like Wagepay in Canada.

5. Woveo: Best for Community-Based Credit Building

Woveo uses a savings-group and community line-of-credit model rather than a standard advance, with access up to about $500. It offers a free plan and a paid premium tier. The structure is different from the other apps here, built around group saving and gradual credit access.

The model works like a shared savings circle. You contribute regularly and build a track record that unlocks credit access over time. That setup rewards consistency over speed. It is not the fastest way to get cash today, but it can suit someone building a savings habit alongside a small safety net rather than reacting to an urgent shortfall.

Pros:

- Community-based model with a free plan

- Combines saving and credit access

Cons:

- Slower than a direct advance

- The group structure does not suit urgent needs

Who it's for: Canadians who want to build savings and credit together and are not in a rush for funds.

6. Cash Money: Best When You Need More Than an App Advance

Cash Money is a regulated short-term lender, not a cash advance app, with amounts ranging well above what any app offers. It fills the gap when you need more than an app can advance. The cost is the catch. A payday-style loan can charge up to the federal maximum of about $14 per $100 borrowed, which works out to roughly 365% a year.

Treat this as a last resort. The cost is far higher than a cash advance app, and it climbs fast the longer you carry it.

Pros:

- Access to larger amounts than any app

- Established, regulated lender

Cons:

- Payday-style rates near 365% APR, far above an app advance

- Much more expensive than an interest-free advance

Who it's for: Canadians who need an amount no app can cover and understand the higher cost. Before going this route, read our guide to payday loan alternatives.

NotchUp vs Bree: Which Should You Choose?

Choose Bree if you want a $0 mandatory cost, up to $750, and acceptance of government benefits as income. Choose NotchUp if you need up to $1,500 or you want to advance against pure gig or freelance income.

Here is the head-to-head:

- Cost: Bree charges 0% interest with free standard delivery. NotchUp charges a flat $5 on every advance.

- Maximum amount: NotchUp advances up to $1,500. Bree advances up to $750.

- Eligibility: Bree accepts employment income and government benefits (ODSP, OW, CPP, CCB, EI). NotchUp also accepts a broad income range.

- Trust: Bree has 8,007+ Trustpilot reviews at 4.8 out of 5 and 600,000+ users. NotchUp has a thin, mixed review history.

- Availability: Bree serves Canadians broadly. NotchUp's licence is centred in British Columbia.

NotchUp genuinely wins on the maximum amount and on advancing against gig income alone. For most Canadians who want the lowest cost, a proven app, and benefit-income acceptance, Bree's instant cash advance is the better daily-use choice.

How to Choose the Right Cash Advance App

The right app depends on four things: how much you need, where your income comes from, how fast you need it, and what it really costs. Match the app to your situation rather than chasing the highest advertised limit.

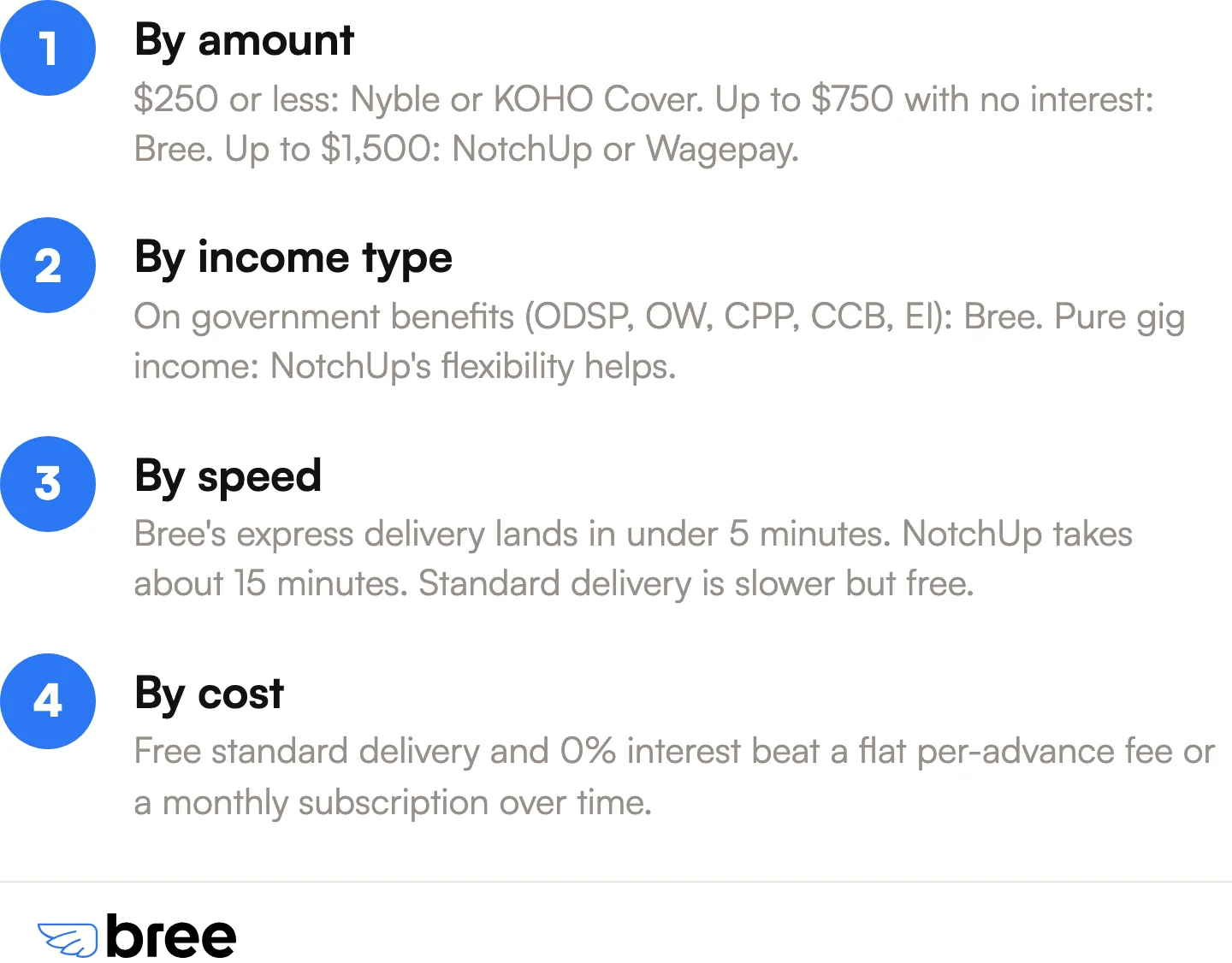

- By amount: Need $250 or less? Nyble or KOHO Cover work. Need up to $750 with no interest? Bree. Need up to $1,500? NotchUp or Wagepay.

- By income type: On government benefits? Bree accepts ODSP, OW, CPP, CCB, and EI. Pure gig income? NotchUp's flexibility helps.

- By speed: Bree's express delivery lands in under 5 minutes. NotchUp takes about 15 minutes. Standard delivery is slower but free.

- By cost: Free standard delivery and 0% interest beat a flat per-advance fee or a monthly subscription over time.

For most Canadians who want no mandatory cost and benefit-income acceptance, Bree is the natural fit. For larger one-time amounts, NotchUp or a regulated lender may be the answer.

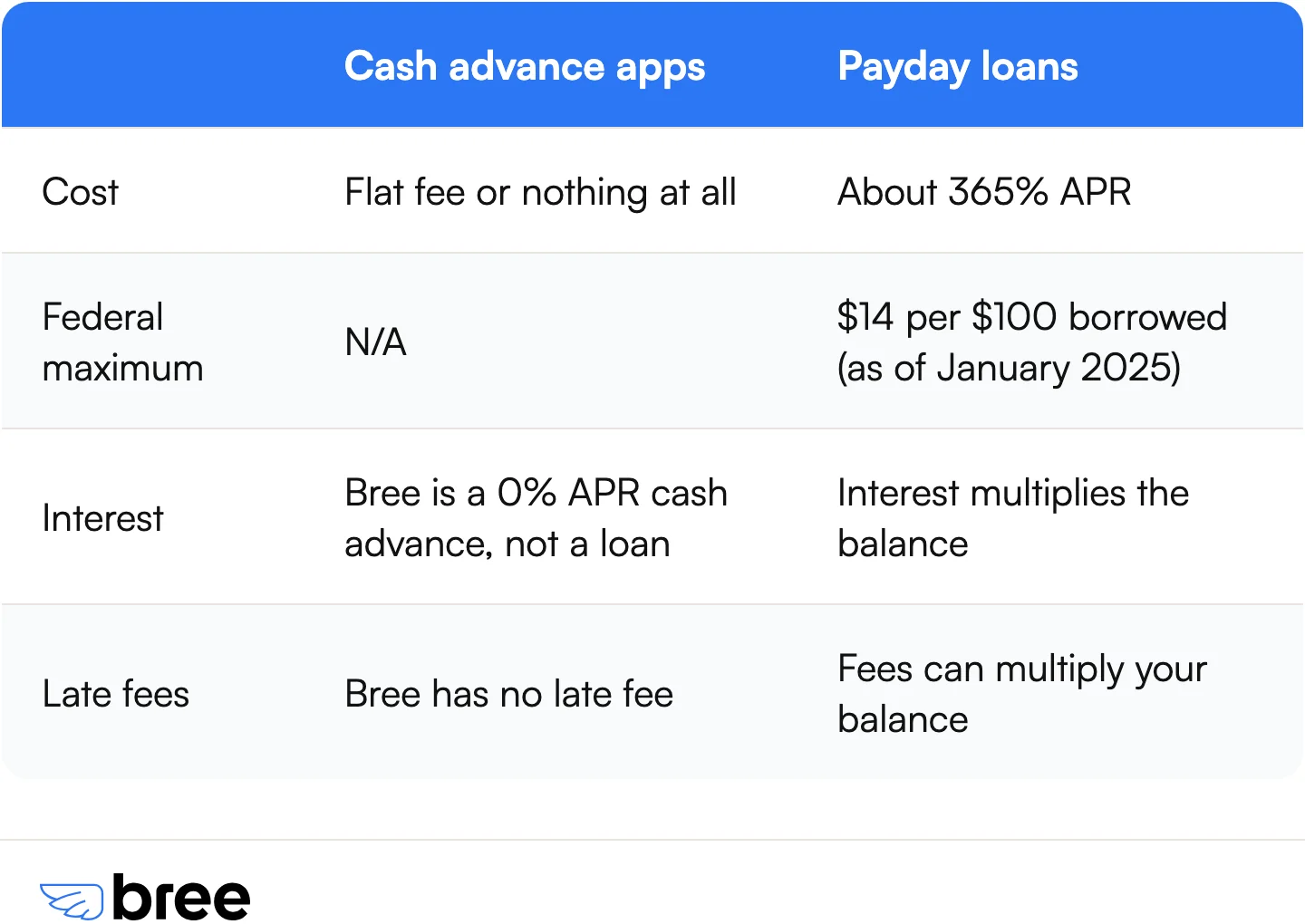

Cash Advance Apps vs Payday Loans

Cash advance apps charge a flat fee or nothing at all, while a payday loan in Canada can cost about 365% APR. As of January 2025, the federal maximum is $14 per $100 borrowed, which works out to roughly 365% a year on a two-week loan, according to the Financial Consumer Agency of Canada. That gap is the whole reason these apps exist. Bree, for example, is a 0% APR cash advance, not a loan, so there is no interest and no late fee to multiply your balance.

The risk to watch with any advance is the borrowing cycle. PBS NewsHour reported on the costs and pitfalls of earned wage access apps, noting that small per-advance fees are proportionally high and that repeat borrowing can shrink each paycheque and prompt the next advance. An interest-free model with no late fees and no mandatory cost is the least likely to dig that hole.

With 85% of Canadians living paycheque to paycheque, the difference between a 0% advance and a 365% loan is real money. If you are trying to break a payday cycle, start with our 3 steps to escape the payday loan debt cycle.

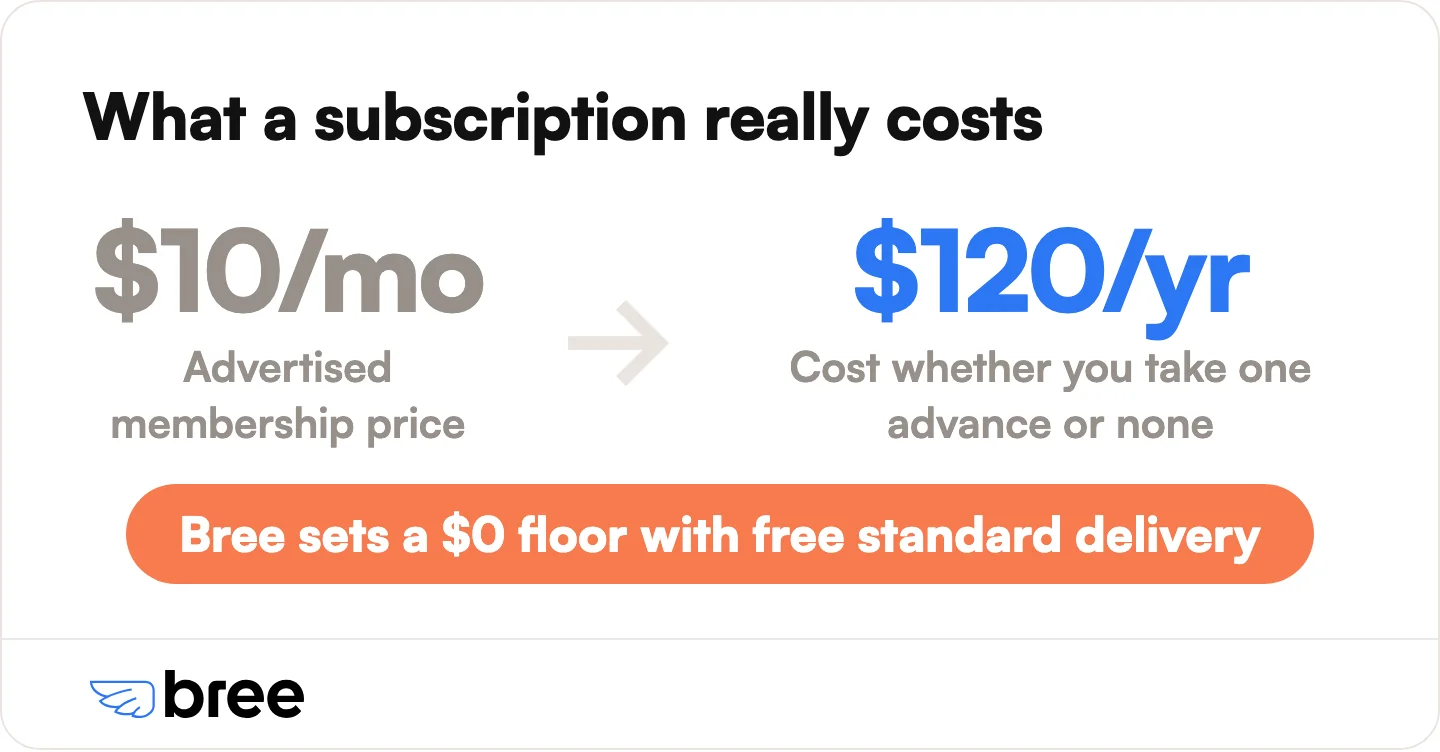

Watch the Real Cost: Fees, Subscriptions, and "Optional" Tips

The advertised price of a cash advance app is rarely the full price. Three costs hide in the fine print: per-advance fees, monthly subscriptions, and pre-selected tips.

A flat $5 per advance, like NotchUp's, looks small until you borrow twice a month and pay $120 a year. Subscription apps are worse in slow months, because they bill you every month even when you borrow nothing. A $10 monthly membership costs $120 a year whether you take one advance or none. And some apps pre-select an "optional" tip during checkout, quietly turning a free advance into a paid one.

Bree's model avoids these traps. Standard delivery is free, which sets a $0 floor on cost. The membership is optional and can be bypassed, and tips are genuinely optional with no pre-selected amount. Before you commit to any app, read the fee screen carefully and check whether a subscription renews whether you borrow or not.

Frequently Asked Questions

How can I get $50 or $100 instantly in Canada?

A cash advance app is the fastest way to get $50 or $100 instantly in Canada with no credit check. Bree's express delivery sends funds to your connected debit card in under 5 minutes. For a step-by-step walkthrough, see our guide to borrowing $50 instantly in Canada.

How can I get $200 instantly?

You can get $200 instantly through a cash advance app that approves you on bank history rather than credit score. Bree advances up to $750, so $200 is well within range, with express delivery in minutes. See our guide to $200 advances with fast approval in Canada.

Can I use Bree if I'm on EI or ODSP?

Yes. Bree accepts government benefits as qualified income, including EI, ODSP, OW, CPP, and CCB. You do not need traditional employment to qualify. This is a key difference from apps that accept employment income only. For more on timing advances around benefit dates, see our ODSP payment dates guide.

Do apps like NotchUp check your credit?

No. NotchUp, Bree, Nyble, KOHO Cover, and the other apps on this list do not run a credit check. Approval is based on your bank account transaction history, usually the last two months of deposits. This is why they work for people with limited or damaged credit.

What's the highest amount these apps advance?

NotchUp and Wagepay advance up to $1,500, the highest among app-based options. Bree advances up to $750 with 0% interest, which is higher than Nyble and KOHO Cover at $250. Regulated lenders like Cash Money offer larger amounts but at a much higher cost.

Are cash advance apps safe in Canada?

Cash advance apps are regulated provincially in Canada, and the reputable ones use bank-grade security. Before you sign up, check for 2048-bit encryption, read-only bank access that cannot move money without your request, and a strong, verifiable review history. Bree uses read-only access and holds a 4.8 out of 5 Trustpilot rating across 8,007+ reviews.

Is there a Canadian version of Dave or Earnin?

Dave and Earnin are US-only apps with no Canadian version. Canadians should use a domestic app instead. Bree, Nyble, and NotchUp all offer cash advances built for the Canadian banking system and Interac e-Transfer.

The Bottom Line

The best apps like NotchUp in Canada are Bree, Nyble, and KOHO Cover, and for most Canadians, Bree is the strongest pick. It costs nothing in interest or late fees, advances more than the $250 apps, and accepts income that other apps reject.

Bree is the interest-free cash advance app that accepts government benefits as income and has served 600,000+ Canadians. NotchUp still makes sense if you need up to $1,500 or you are advancing against gig income alone, and a regulated lender can cover amounts no app will. But the everyday choice for a no-cost, no-credit-check advance is clear.

If you want cash between paycheques without interest, late fees, or a credit check, you can get up to $750 with Bree and sign up at app.trybree.com/register.

Sources

- Finder Canada: NotchUp review

- Finder Canada: Cash advance apps comparison

- PBS NewsHour: The costs and pitfalls of earned wage access apps

- Financial Consumer Agency of Canada: Payday loans

- Statistics Canada: Ability to cover an unexpected $500 expense

- H&R Block Canada: Canadians living paycheque to paycheque

Join our newsletter to get the latest updates

.png)