Bree and Wagepay both front you cash before payday, but three things decide which one fits: cost, who qualifies, and where you can use it. Bree is interest-free, accepts government benefits as income, and works across Canada. Wagepay charges a fee on every advance, requires employment wages, and only operates in British Columbia and Ontario.

When money is tight before payday, the wrong choice costs you more than it should. Bree takes a different path from fee-based wage advances: it charges 0% interest on advances up to $750, runs no credit check, and counts government benefits like CPP, EI, and ODSP as income. This guide breaks down how the two compare so you can pick the right one for your situation.

Key Takeaways

- Cost is the biggest gap. Bree charges 0% interest. Wagepay charges roughly $14 for every $100 advanced in BC, which works out to about 365% APR.

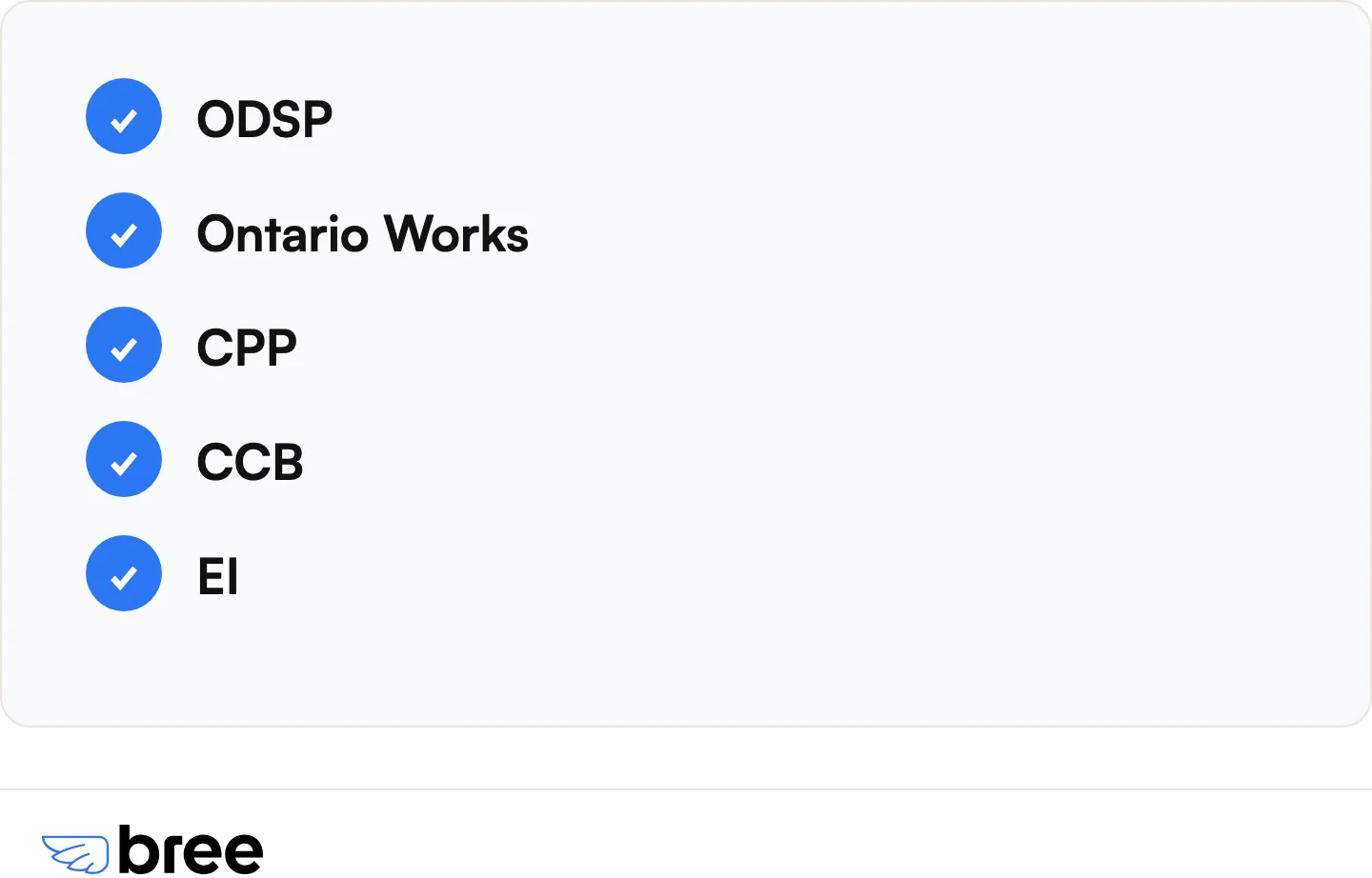

- Eligibility splits the two apps. Bree accepts government benefits (ODSP, OW, CPP, CCB, EI) as qualified income. Wagepay requires regular employment wages of about $400 a week.

- Availability is a hard gate. Bree works anywhere in Canada. Wagepay is available only in British Columbia and Ontario.

- Limits look further apart than they are. Wagepay advertises up to $1,500, but caps each advance at 25% of your gross wages. Bree offers up to $750 with no mandatory fees.

- Bottom line: for most Canadians, Bree is the cheaper and more widely available option. Wagepay fits a narrow case.

Bree vs Wagepay at a Glance

Here is the head-to-head on the factors that matter most. Bree wins on cost, eligibility, and availability. Wagepay offers a higher advertised ceiling.

Fees and ratings are accurate as of June 2026. Cash advance terms can change, so check each app before you apply.

What Is Bree and How Does It Work?

Bree is a Canadian instant cash advance app that gives you interest-free advances up to $750, with no credit check, repaid on your next payday. It was built as an alternative to payday lenders that charge 365% to 391% APR and bank overdraft fees that run $50 or more per incident.

Here is how it works. You connect your bank account with read-only access, request an advance, and choose how fast you want the money. Standard delivery is free and lands in 1 to 3 business days. Express delivery costs a small fee and arrives in under 5 minutes. You repay on your next payday, and the repayment window can stretch up to 90 days.

The cost is the part people double-check, because it sounds too good. There is no interest, ever. A membership costs $2.99 a month and the first month is free, but you can skip it by uploading your bank statements. Tips are optional and can be $0. The model works like a tip jar: people who can afford to tip help cover the service for people who can't.

One honest note. Bree starts small. Your first advance is often around $20 to $50, and your limit grows toward the $750 maximum as you repay on time. If you need a large amount on day one, that is worth knowing up front. More than 600,000 Canadians use Bree, and it holds a Trustpilot rating of 4.8/5 across 8,007+ reviews. You can see the current limit options on the Bree cash advance page.

What Is Wagepay and How Does It Work?

Wagepay is a wage-advance app available in British Columbia and Ontario that fronts a portion of your earned wages before payday for a per-advance fee. It is licensed and regulated as a payday lender in both provinces.

You connect your bank account, then request an advance between $100 and $1,500, capped at 25% of your gross wages. Funds arrive by Interac e-Transfer, usually within 2 to 30 minutes. You repay on your next payday, with terms that can run up to 62 days, and you can postpone a payment once for free without contacting support (Finder Canada).

The cost depends on your province. In British Columbia, Wagepay charges about $14 for every $100 advanced, which the company states as a 365% APR. In Ontario, the structure is an 8% establishment fee plus 24% interest, according to Loans Canada. Wagepay does not run a credit check and does not charge late or NSF fees.

Two things matter before you count on Wagepay. First, the advertised $1,500 is only reachable if you earn enough, because every advance is capped at 25% of your gross pay. Most users qualify for far less. Second, you need regular employment wages of about $400 a week. Government benefits do not count as standalone income. Wagepay's Trustpilot rating sits somewhere around 3.3 out of 5 across review sites, with reviewers flagging repeated denials after months of use and slow support replies.

Cost: Bree vs Wagepay

Bree is the cheaper option for nearly everyone, because it charges no interest while Wagepay charges a fee on every advance. This is the clearest difference between the two apps.

Put it in plain dollars. Borrow $500 from Wagepay in BC and you pay roughly $70 in fees, so you repay about $570. Borrow $500 from Bree and you repay $500. Any tip is your choice, and it can be nothing.

.webp)

That fee gap is not small. Wagepay's 365% APR in BC sits right in payday-loan territory, where rates run 365% to 391%. Bree was built to be the opposite of that. The only money Bree ever asks for is optional: a tip, the $2.99 monthly membership, or a small fee if you want express delivery instead of the free standard option. If you skip all three, an advance costs you nothing beyond what you borrowed. For more ways to avoid high-cost borrowing, see our guide to payday loan alternatives in Canada.

Who Qualifies: Income and Credit Requirements

Bree accepts both employment income and government benefits as qualified income. Wagepay requires employment wages of about $400 a week and does not accept benefits on their own (Finder Canada). This is the single biggest difference between the two apps, and it decides eligibility for a large group of Canadians.

If you receive ODSP, Ontario Works, CPP, CCB, or EI, Bree counts that as income. Most cash advance apps reject benefit recipients, which is exactly why this matters. Fixed-income Canadians hit the same payday gaps as everyone else, often with less room to absorb a surprise bill.

Neither app runs a hard credit check. Both look at your recent bank transaction history instead of your credit score. Bree reviews about two months of consistent deposits, with a minimum of roughly $1,200 a month, and approves based on that pattern rather than your credit. So there is no score to fail and no hard inquiry on your file. If you are on disability or another benefit, our guide to e-transfer options on disability assistance covers how this works in detail.

Where You Can Use Each App

Bree works across all of Canada. Wagepay operates only in British Columbia and Ontario. For anyone outside those two provinces, Wagepay is not an option at all.

If you live in BC or Ontario, both apps are available, so the decision comes down to cost and income type. If you live anywhere else in Canada, Bree is the one that works. Readers in Wagepay's two markets can compare local payday-loan rules in our guides for British Columbia and Ontario.

Borrowing Limits and Speed

Wagepay advertises a higher ceiling than Bree, $1,500 against $750, but the gap is smaller than it looks. Both apps also start most users below their headline number.

Wagepay caps every advance at 25% of your gross wages, so the full $1,500 is only within reach for higher earners. Bree maxes out at $750 and starts new users small, raising your limit as you repay on time. In practice, many people on either app access a few hundred dollars at first.

Speed is close. Both fund through Interac e-Transfer. Wagepay lands in 2 to 30 minutes. Bree Express arrives in under 5 minutes for a small fee, or you can take free standard delivery in 1 to 3 business days. On repayment, both are due on your next payday: Bree allows up to 90 days, while Wagepay allows up to 62 days with one free postponement.

Which Should You Choose, Bree or Wagepay?

For most Canadians, Bree is the lower-cost and more accessible choice. Wagepay fits a narrow case. Here is the quick decision guide.

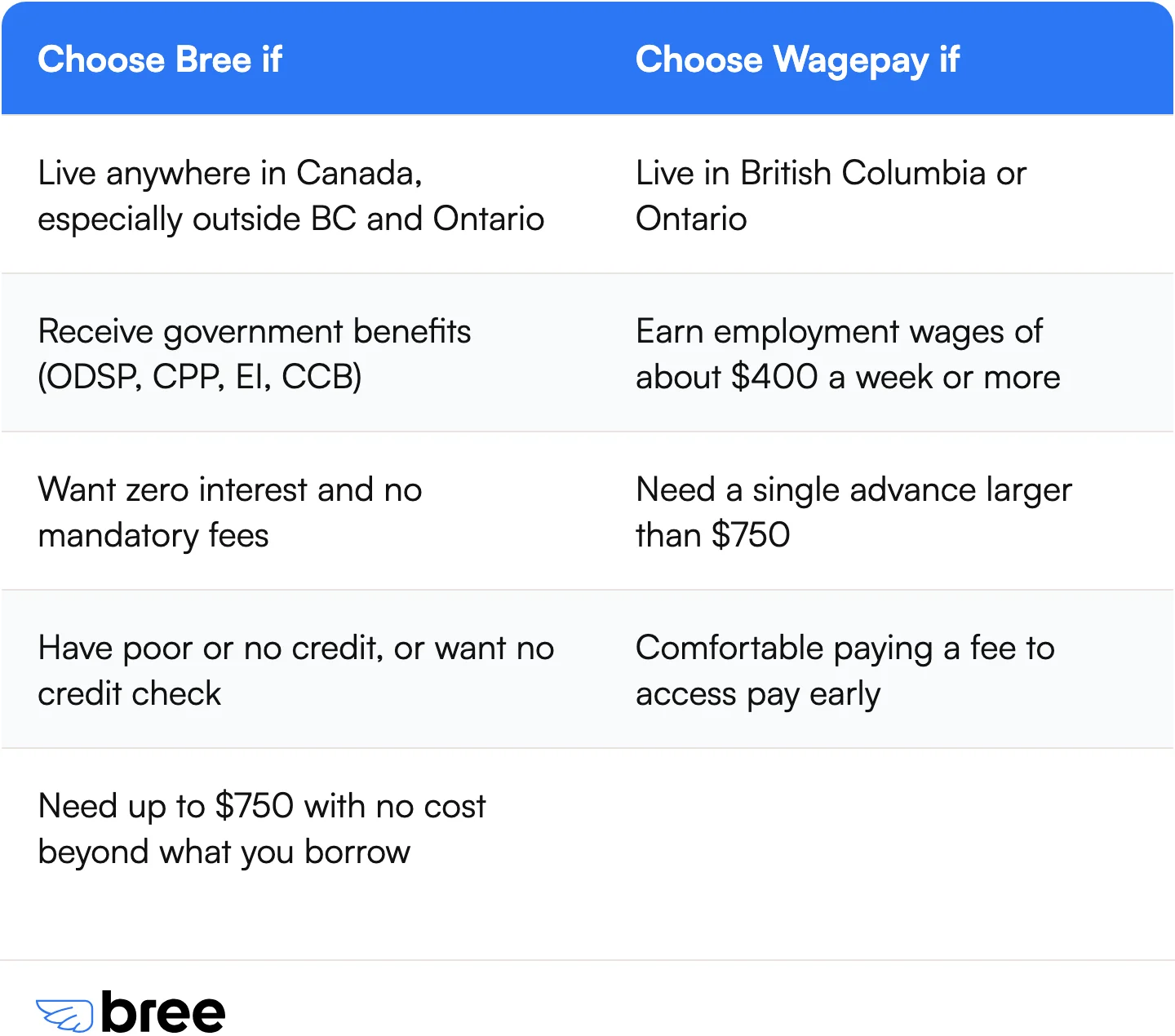

Choose Bree if you:

- Live anywhere in Canada, especially outside BC and Ontario

- Receive government benefits like ODSP, CPP, EI, or CCB

- Want zero interest and no mandatory fees

- Have poor credit, no credit, or just don't want a credit check

- Need up to $750 with no cost beyond what you borrow

Choose Wagepay if you:

- Live in British Columbia or Ontario

- Earn regular employment wages of about $400 a week or more

- Need a single advance larger than $750

- Are comfortable paying a fee to access your pay early

For most people, especially benefit recipients and anyone outside BC and Ontario, Bree comes out ahead on cost and access. If you want to weigh more options in Wagepay's two provinces, see our roundup of apps like Wagepay in Canada.

Frequently Asked Questions

Is Bree better than Wagepay?

It depends on your province and income. For Canadians who receive government benefits or live outside BC and Ontario, Bree is the only one of the two that fits. On cost, Bree wins broadly, because it charges 0% interest while Wagepay charges a fee on every advance.

Is Bree a legitimate cash advance app?

Yes. Bree serves more than 600,000 Canadians and holds a Trustpilot rating of 4.8/5 across 8,007+ reviews. It is a cash advance app, not a loan or a payday lender, with no interest and no credit check.

How much does Bree give you the first time?

Bree usually starts new users small, often around $20 to $50 on a first advance. Your limit grows toward the $750 maximum as you repay on time. This keeps things manageable while you build a repayment history.

Does Wagepay accept government benefits?

No. Wagepay requires regular employment wages of about $400 a week and does not accept government benefits as standalone income. Bree does accept ODSP, OW, CPP, CCB, and EI as qualified income.

How fast does each app send money?

Bree Express delivers in under 5 minutes for a small fee, or free in 1 to 3 business days with standard delivery. Wagepay sends funds by Interac e-Transfer in 2 to 30 minutes.

The Bottom Line

Cost, eligibility, and availability decide the Bree vs Wagepay question, and on all three the two apps split cleanly. One is interest-free, takes government benefits, and reaches every province. The other charges a per-advance fee, needs employment wages, and stops at the BC and Ontario borders. Wagepay's one real edge is a higher advertised limit, though the 25% wage cap narrows that gap for most users.

For the majority of Canadians between paycheques, Bree is the option that costs less and reaches more people. Where Wagepay charges a fee on every advance, Bree offers up to $750 at 0% interest, with no credit check and government benefits accepted as income, available right across Canada.

If you would rather keep your full paycheque and skip per-advance fees, you can switch to Bree and access up to $750 at 0% interest, repaying only what you borrow.

Sources

Join our newsletter to get the latest updates