Looking for loans like NoJuice? The best options are not loans at all. They are instant cash advance apps that match NoJuice's same-day speed and skip the credit check, and some cost less or go higher than NoJuice's $500.

NoJuice is a Canadian cash advance app that advances up to $500 the same day with no credit check. That makes it a solid pick. But it is not the only one, and depending on what you need, it may not be the best one for you.

Bree is our interest-free cash advance app, trusted by more than 600,000 Canadians. We advance up to $750 with no credit check and 0% interest, and we accept government benefits as income, which most apps reject. That higher limit is the main reason people looking for a NoJuice alternative land on Bree. Below we compare five apps like NoJuice, ranked by who each one fits, with the interest-free options first.

Key Takeaways

- Apps like NoJuice are cash advances, not loans. You pay 0% interest with an app like Bree, versus the roughly 391% APR that payday-style e-transfer lenders charge for similar same-day money.

- Bree raises the ceiling to $750. That is a higher no-credit-check limit than NoJuice's $500, and it is still interest-free.

- NotchUp goes highest at $1,500 for a flat $5 fee, so it is the pick when you need more than any 0% app offers.

- Government benefits count as income with Bree. ODSP, Ontario Works, CPP, CCB, and EI all qualify, while most apps require a regular paycheque.

- The bank NSF fee is now capped at $10 as of March 2026, down from about $45 to $48. An app still helps you dodge that fee, plus the penalties a bounced payment can trigger.

Quick Comparison: Apps Like NoJuice

Amounts and costs are accurate as of July 2026 and can change.

What NoJuice Offers & Where These Apps Do More

NoJuice advances up to $500 the same day with no credit check and no hidden fees. For a small, fast gap before payday, it does the job. The reason people still shop around is that $500 is a hard ceiling, and a few apps do more for the same kind of borrower.

Three gaps are worth knowing about. First, the limit: Bree advances up to $750 and NotchUp up to $1,500, so you are not capped at $500 when a bill runs higher. Second, the cost model: the strongest apps charge 0% interest rather than a percentage fee. Third, income: Bree counts government benefits, so people on ODSP, EI, or CPP can qualify where a paycheque-only app would decline them.

For a wider look at this category, see our guide to the best cash advance apps in Canada. Below, each pick is scored on limit, cost, funding speed, and who it actually fits.

The 5 Best Apps Like NoJuice

Here are five apps like NoJuice, ranked by who each one suits. We lead with the interest-free options because they cost the least, then cover the higher-limit and wage-advance choices for people who need something different.

1. Bree: Best for the Highest Interest-Free Limit

Bree is our interest-free cash advance app, built in Vancouver and used by more than 600,000 Canadians. We advance up to $750 with no credit check at all, not even a soft pull. Because Bree is a cash advance and not a loan, there is no interest and nothing building against your credit.

The $750 ceiling is the headline against NoJuice, and no other 0% app here comes close: KOHO and Nyble cap at $250, and NotchUp only reaches $1,500 by charging a fee. If your gap is bigger than $500, we cover it without pushing you toward a pricier product. We approve you on about two months of bank account history, and we accept both employment income and government benefits, including ODSP, Ontario Works, CPP, CCB, and EI. Express delivery reaches your debit card in under five minutes, and standard delivery is free within one to three business days.

The cost is simple: Bree is free to use, with no interest, ever. There is nothing you have to pay to get an advance. You can leave a voluntary tip the way you would tip a waiter, and tips from people who can afford them help cover the service for those who cannot. The only other optional cost is an express fee if you want your cash in minutes rather than waiting for free standard delivery. Bree holds a 4.8 out of 5 rating on Trustpilot from more than 8,007 reviewers, and bank access is read-only, so we can read your history but cannot move money without your request.

- Pros: 0% interest, the highest no-credit-check limit here at $750, accepts government benefits, funds in under five minutes.

- Cons: Maxes at $750, so it will not cover a large purchase. You need recurring deposits of at least about $1,200 a month.

- Not for you if: you need more than $750 in one advance, or your income is a one-off rather than a steady deposit.

Ready to move past NoJuice's $500 cap? Get up to $750 with 0% interest from Bree.

2. NotchUp: Best for the Largest Single Advance

NotchUp is a Canadian earned-wage-access app that advances up to $1,500, the highest limit on this list. It charges a flat $5 fee per advance rather than interest, and funds usually arrive by Interac e-Transfer within about 15 minutes.

The flat fee is the appeal. Five dollars on a larger advance works out cheaper than a percentage-based payday fee, and NotchUp accepts several income types, not just a single employer paycheque. If your shortfall is closer to $1,000 than $200, this is the app that can cover it in one shot.

The trade-off is track record. NotchUp is newer, and its Trustpilot review base is small and mixed, with only a couple dozen reviews at the time of writing. That is thin proof compared to the established apps here, so it is worth reading recent reviews before you rely on it.

- Pros: Highest limit at $1,500, flat $5 fee instead of interest, fast e-Transfer, flexible on income type.

- Cons: Not truly free, and the review history is short and uneven.

- Not for you if: you want a genuinely $0 option, or you prefer an app with a long, proven track record.

We compare more options in our roundup of apps like NotchUp.

3. KOHO Cover: Best for a Built-In Overdraft Cushion

.jpg)

KOHO Cover is a cash advance feature inside KOHO, a Canadian prepaid card and spending app. It advances up to $250 at 0% interest, with no credit check, and works as an overdraft-style cushion built right into the app you already spend from.

If you use KOHO for day-to-day banking, Cover is convenient because it lives where your money already is. It carries about a 4 out of 5 rating on Trustpilot across more than 2,000 reviews, which is a solid record for a banking app. The catch is that you need a KOHO account on a paid plan to use it, and the $250 cap is the lowest ceiling here alongside Nyble.

- Pros: 0% interest, no credit check, convenient if you already bank with KOHO.

- Cons: $250 limit, requires a KOHO account and a paid plan.

- Not for you if: you need more than $250, or you do not want to move your banking into a new app.

For a closer look, read our KOHO review and top alternatives.

4. Nyble: Best for Building Credit as You Borrow

Nyble is a Canadian credit-building line of credit that advances up to $250 at 0% interest with no hard credit check. What sets it apart is that it reports your payments to Equifax, so borrowing small amounts and repaying on time can nudge your credit up over months.

That credit reporting is the reason to pick Nyble over a plain advance. It is well regarded, holding a 4.8 out of 5 on Trustpilot. The free tier funds in one to three business days, while a paid tier around $12 a month adds instant transfers. The limits are the same $250 as KOHO, so this is a small-gap tool, not a rent-sized one.

- Pros: 0% interest, reports payments to help build credit, no hard credit check.

- Cons: $250 cap, and free funding is slow unless you pay for the instant tier.

- Not for you if: you need a larger amount, or you need same-day money without paying for the premium plan.

See how it stacks up in our Nyble versus Bree comparison.

5. Wagepay: Best for Drawing Wages You Have Already Earned

.jpg)

Wagepay is a Canadian wage-advance app that lets you pull money you have already earned, up to $1,500 or about 25% of your gross pay. The higher ceiling suits salaried workers who just need their pay a little early.

The cost is where it differs from the 0% apps. Wagepay charges a fee per advance that lands in payday-fee territory, not a flat or interest-free rate, so a bigger draw costs more. It runs no credit check but needs steady employment wages, which rules out people on benefits. Its Trustpilot score sits at about 3.7 out of 5, lower than the other established apps here, with some reviewers flagging approval and support issues.

- Pros: Higher amount than most apps, no credit check, quick once approved.

- Cons: Charges a percentage-style fee instead of 0%, employment income required, availability is limited by province.

- Not for you if: your income comes from government benefits, or you want a genuinely interest-free advance.

We break down more choices in our roundup of apps like Wagepay in Canada.

Why a 0% Cash Advance App Beats a Payday-Style E-Transfer Loan

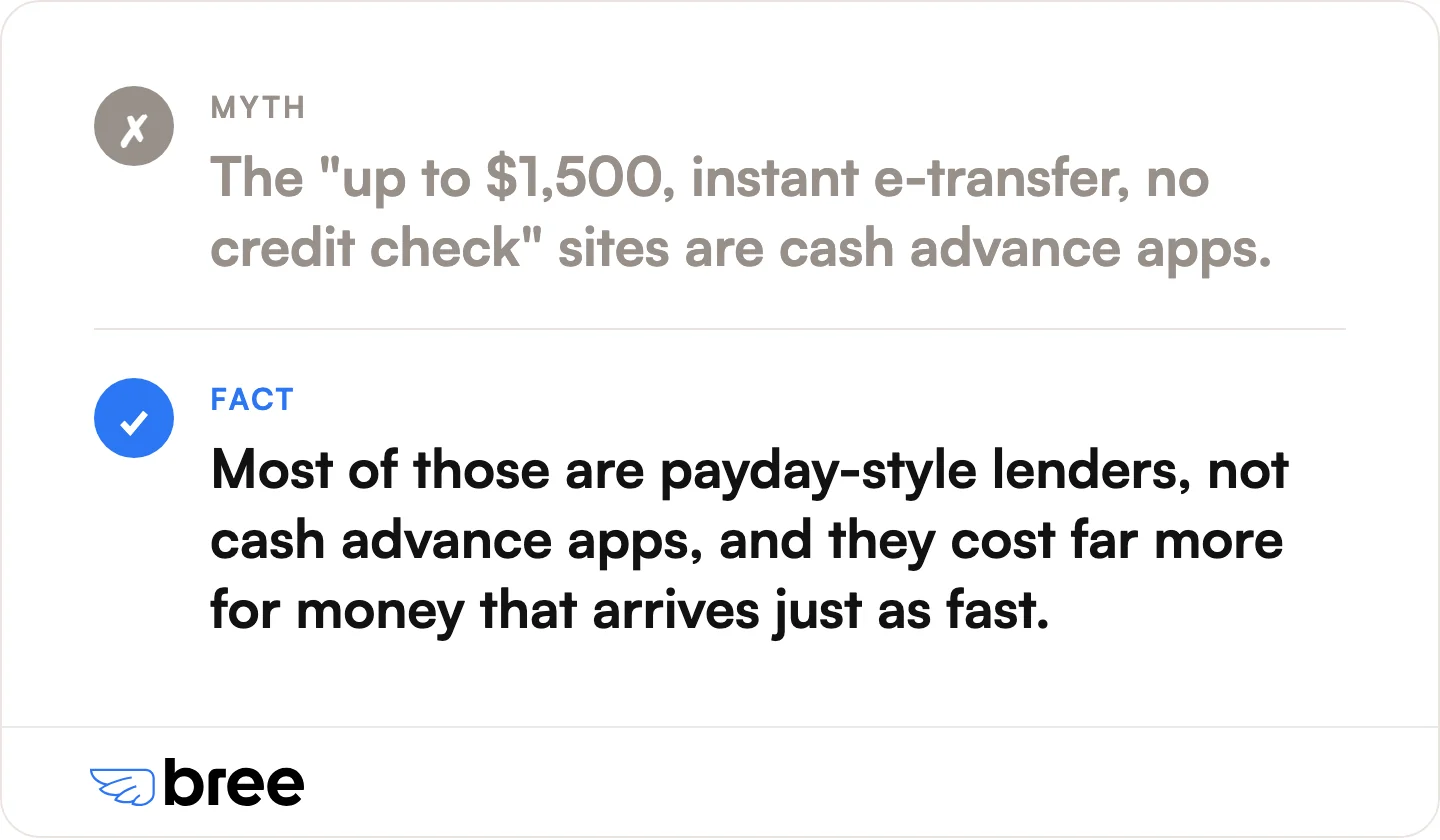

Search for loans like NoJuice and you will see sites promising "up to $1,500, instant e-transfer, no credit check." Most of those are payday-style lenders, not cash advance apps, and they cost far more for money that arrives just as fast.

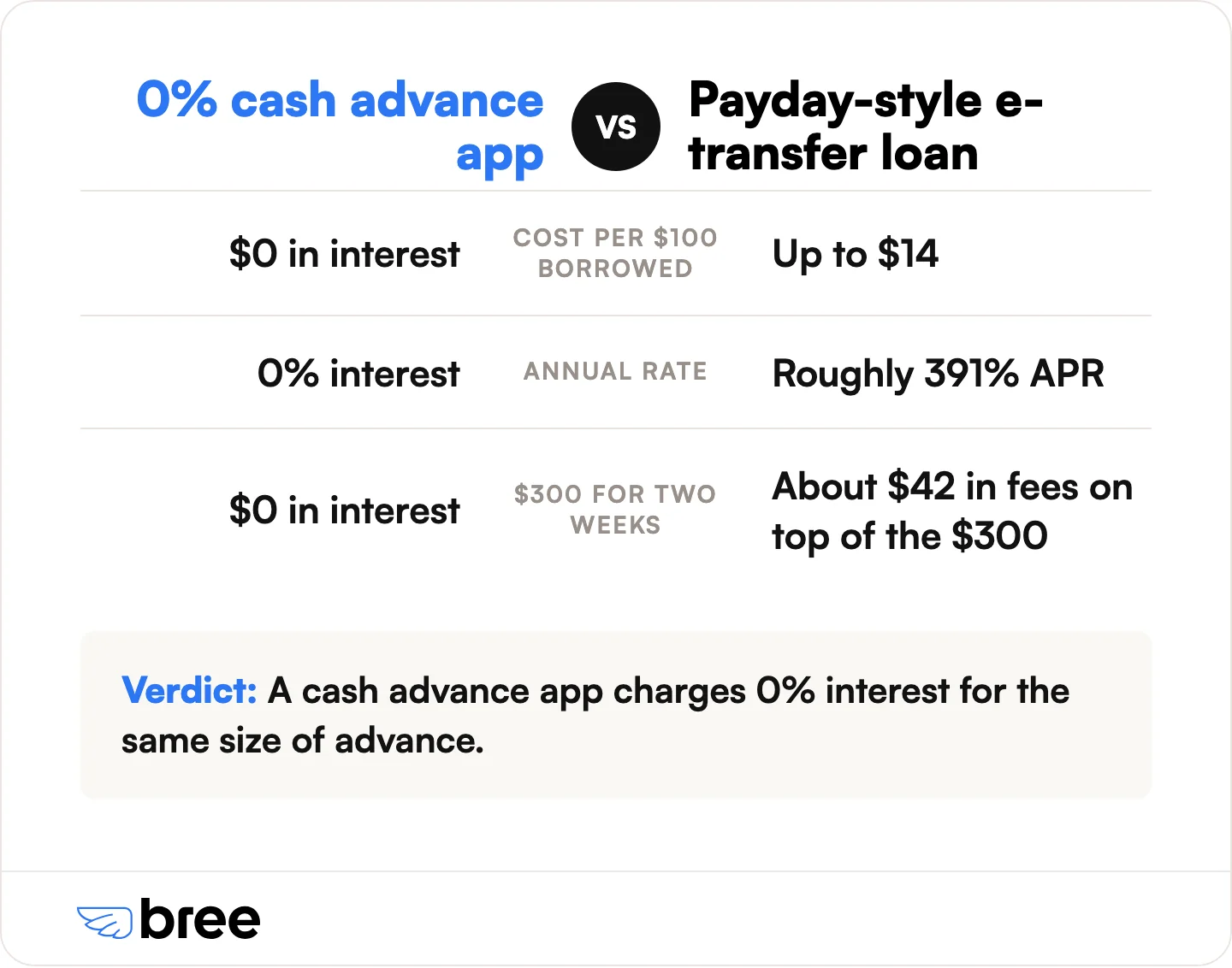

A payday loan can cost up to $14 for every $100 you borrow. According to the Financial Consumer Agency of Canada, that works out to roughly 391% APR, and the criminal interest-rate cap on other lending is now 35%. A cash advance app charges 0% interest for the same size of advance.

The gap is easy to see in dollars. Borrow $300 for two weeks from a payday-style lender at $14 per $100 and you owe about $42 in fees on top of the $300. Take the same $300 as an interest-free advance and the interest is $0. Bree is free, and the only costs are optional: a voluntary tip you set yourself, and an express fee if you want the cash in minutes.

The bigger risk is the debt cycle. A payday loan is due in full on your next payday, and once you repay it you are often short again, so you borrow again to bridge the next two weeks. The Financial Consumer Agency of Canada warns that this pattern traps borrowers as missed payments and penalties stack up. If a payment bounces, your bank can add an NSF fee on top.

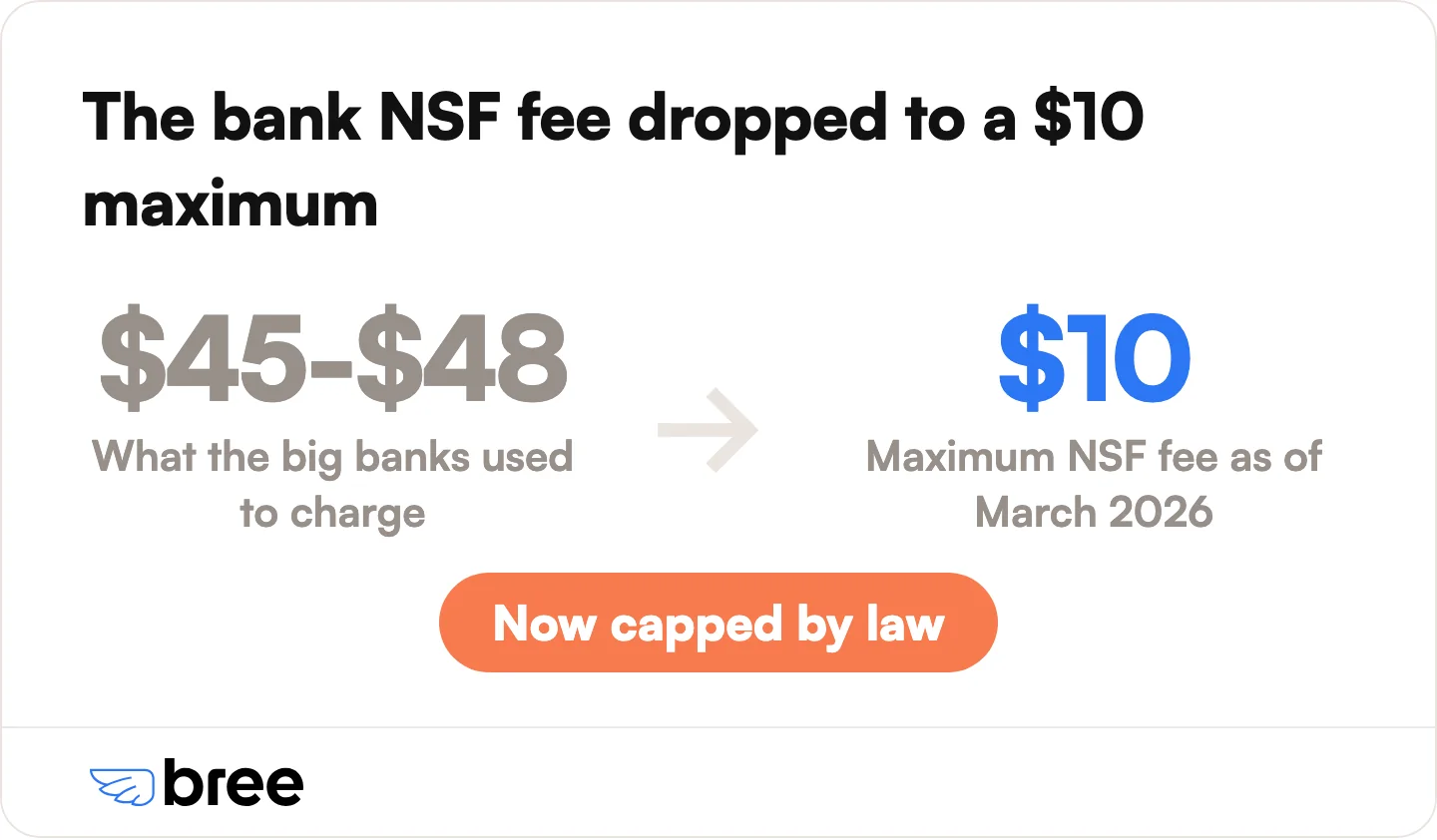

That NSF fee is smaller than it used to be. As of March 2026, federally regulated banks cannot charge more than $10 for a non-sufficient funds fee, down from the $45 to $48 the big banks used to charge, per the Government of Canada. A $10 cap is real relief, but a bounced auto-payment can still trigger lender penalties and a missed bill, which is exactly what a 0% advance helps you avoid. For a fuller list of safer options, see our guide to payday loan alternatives in Canada.

Can I Get an App Like NoJuice With Bad Credit or on Benefits?

Yes. Every app in this list skips the credit check and approves you on your bank account history instead, and Bree also accepts government benefits as income.

If your credit is damaged or thin, that does not block you here. Bree, NotchUp, KOHO Cover, Nyble, and Wagepay all approve based on the deposits landing in your account, not a credit score. There is no hard or soft pull. What they look for is steady income coming in, which is often enough to get approved when a bank or a traditional lender would say no. For more detail, see our guide to cash advances with no credit check in Canada.

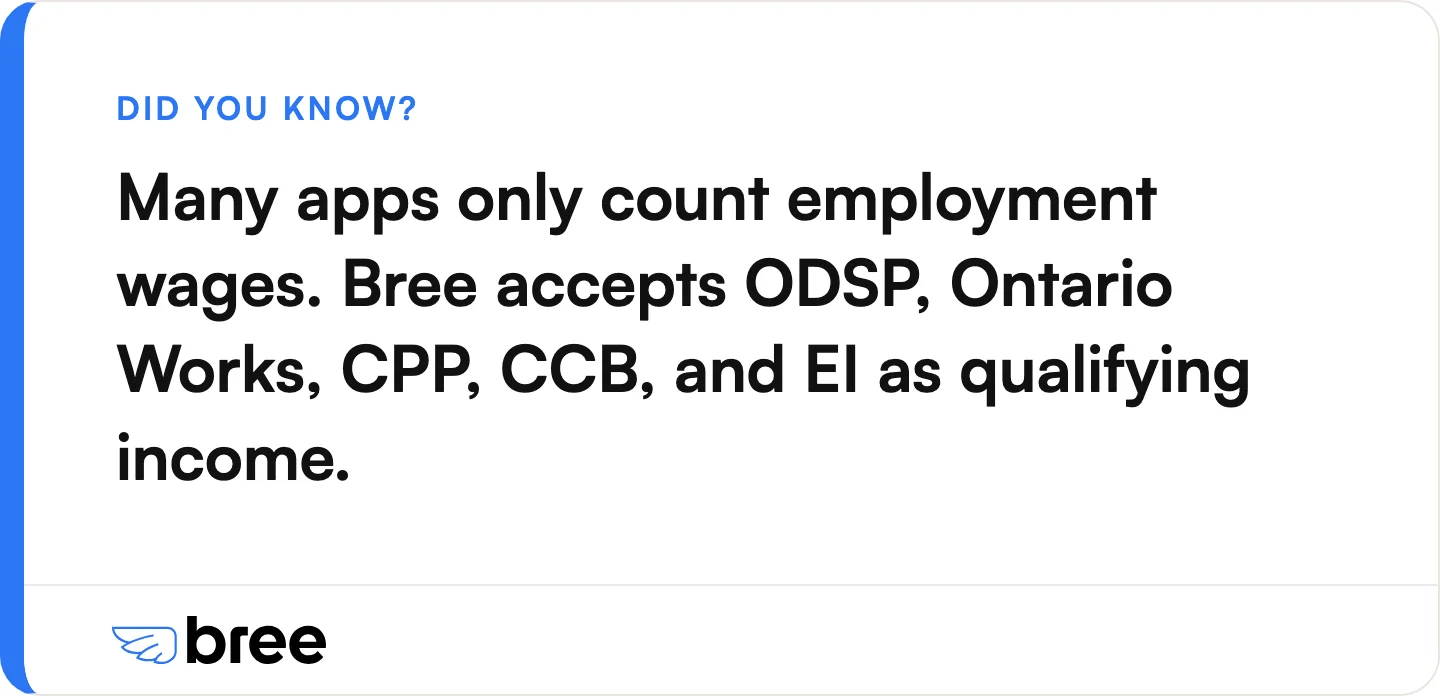

Where your income comes from matters just as much. Many apps only count employment wages, which shuts out anyone on a fixed benefit. Bree accepts ODSP, Ontario Works, CPP, CCB, and EI as qualifying income. If your money arrives as a benefit rather than a paycheque, that acceptance can be the difference between approval and rejection. People tracking a payment can check our ODSP payment dates guide to see when the next deposit lands.

How to Choose an App Like NoJuice

Match the app to your situation rather than picking the first one you see:

- Want it interest-free? Choose a 0% cash advance app: Bree, KOHO Cover, or Nyble.

- Need more than $750? NotchUp advances up to $1,500 for a flat $5 fee.

- On government benefits? Bree accepts ODSP, Ontario Works, CPP, CCB, and EI.

- Building credit? Nyble reports your on-time payments to Equifax.

- Salaried and want your pay early? Wagepay lets you draw wages you have already earned.

Applying is quick with any of them. You connect your bank account or verify your income, choose your amount, pick standard or express delivery, and repay on your next payday. With an interest-free app, you repay only what you borrowed.

Also read: Bree vs Wagepay

Frequently Asked Questions

What app gives you $500 instantly in Canada?

Several cash advance apps fund $500 the same day. NoJuice advances up to $500, and Bree advances up to $750 with Express delivery reaching your debit card in under five minutes. Both skip the credit check, so approval comes down to your bank account history rather than your credit score.

What's the easiest cash advance app to get approved for?

Apps with no credit check are the easiest to qualify for. Bree, KOHO Cover, and Nyble approve you on your banking history, not your credit file, so a low or thin credit score does not stop you. Bree also accepts government benefits, which widens who can get approved.

Are there apps like NoJuice with no credit check?

Yes. Every app in this roundup runs no credit check at all. Bree, NotchUp, KOHO Cover, Nyble, and Wagepay all approve based on the deposits in your bank account, so there is no hard or soft pull on your credit.

Can I get a cash advance without a regular paycheque?

Yes, with Bree. It accepts government benefits, including ODSP, Ontario Works, CPP, CCB, and EI, as qualifying income. Most apps require employment wages, so if your income is a benefit rather than a paycheque, Bree is usually the app that will approve you.

How much do apps like NoJuice actually cost?

The interest-free apps cost 0% in interest. Bree is free to use, with no interest and no mandatory fees, only a voluntary tip and an optional express fee for faster funding. NotchUp charges a flat $5 fee, and Wagepay charges a percentage-style fee. Compare that to a payday-style lender at about $14 per $100, or roughly 391% APR, and the app is far cheaper for the same fast money.

The Bottom Line

The best apps like NoJuice are not payday loans. They are interest-free cash advance apps that match the speed people want without the roughly 391% APR that keeps borrowers stuck. NoJuice is a fair $500 option, but if you need a higher limit, a lower cost, or income flexibility, one of these picks will fit you better.

For most Canadians facing a short gap before payday, Bree is the upgrade we would point them to. Our community-supported model keeps advances at 0% interest with only a voluntary tip, we approve most people in under five minutes, and we hold a 4.8 out of 5 Trustpilot rating across more than 8,007 reviews. Add a $750 limit and acceptance of government benefits, and we do more than NoJuice for the same kind of borrower.

If you want fast money without the payday-loan trap, get up to $750 with 0% interest from Bree.

Sources

Join our newsletter to get the latest updates

.png)

.png)